The question of whether Puerto Rico pays taxes often sparks curiosity, revealing a fascinating and complex relationship between the island territory and the United States. For travelers planning an immersive cultural experience, investors eyeing new opportunities, or individuals considering a significant lifestyle change, understanding Puerto Rico’s unique tax structure is paramount. Far from a simple yes or no answer, the reality involves a blend of local taxation, federal exemptions, and targeted incentives designed to spur economic growth, all within the context of Puerto Rico’s status as an unincorporated U.S. territory. This distinct fiscal environment not only shapes the economic landscape but also influences everything from the cost of goods and services to the types of accommodations and lifestyle opportunities available across this vibrant Caribbean gem.

The Unique Tax Landscape of Puerto Rico: An Overview

At the heart of the “does Puerto Rico pay taxes” query lies its distinct political status. As an unincorporated territory of the United States, Puerto Rico occupies a unique position, neither a state nor an independent nation. This status grants its residents U.S. citizenship but places them under a different federal tax regime than residents of the 50 states. This arrangement, rooted in historical legislation such as the Foraker Act of 1900 and specifically codified in Internal Revenue Code Section 933, establishes a fiscal framework that is both exceptional and critically important for anyone engaging with the island’s economy or considering making it their home.

A US Territory with Distinct Fiscal Rules

The primary distinction for Puerto Rico residents is their general exemption from federal income tax on income earned within the territory. This means that individuals who are bona fide residents of Puerto Rico typically do not pay federal income tax to the U.S. Treasury on income sourced from Puerto Rico. This significant departure from the standard U.S. tax system has profound implications, acting as a powerful magnet for both individual investors and service-based businesses looking to optimize their tax liabilities. It’s a cornerstone of the island’s economic development strategy, aiming to attract capital, talent, and entrepreneurial drive. However, it’s crucial to understand that this exemption is not absolute and comes with specific conditions and nuances, particularly for those with income generated outside of Puerto Rico or for individuals who do not meet the strict residency requirements. The allure of this federal income tax exemption is a key factor driving interest in Puerto Rico as a destination for long-term stays, permanent relocation, and business expansion, shaping the island’s lifestyle offerings and investment landscape.

Federal vs. Local: Understanding the Differences

While the federal income tax exemption on Puerto Rico-sourced income is a defining characteristic, it’s vital to recognize that residents are far from tax-free. They are subject to a comprehensive system of local taxes, mirroring many of the obligations faced by residents in the 50 states. This includes paying income taxes to the Puerto Rico Treasury Department – often at rates comparable to, or even higher than, some U.S. states before applying incentives. Beyond local income tax, residents contribute to federal programs like Social Security and Medicare, just like their counterparts in the mainland U.S.. This means individuals and businesses contribute to these national safety nets, ensuring continuity of benefits regardless of their residency within the U.S. sphere.

Moreover, a range of excise taxes, property taxes, sales and use taxes (IVU), and other fees are levied at the local level. These local taxes fund essential public services, infrastructure projects, and support the broader operations of the Puerto Rico government. For instance, the sales and use tax impacts the cost of goods and services, a relevant consideration for travelers budgeting for their trips or residents evaluating the cost of living. Property taxes contribute to local municipalities, affecting real estate investment and the availability of diverse accommodation options, from luxury villas to more budget-friendly apartments. Understanding this dual-tax structure – federal exemption for local income combined with robust local taxation – is fundamental to grasping the full financial picture for anyone interacting with Puerto Rico. It paints a realistic portrait of the financial obligations and benefits that shape the island’s economy, influencing everything from hotel development to the vibrant local culinary scene.

Unlocking Economic Incentives: Act 60 and Its Predecessors

In an ambitious effort to revitalize its economy and attract new investment, Puerto Rico has historically implemented a series of tax incentive laws. These initiatives, most notably the now-consolidated Act 60, are designed to draw businesses and high-net-worth individuals to the island, promising significant tax advantages in exchange for contributing to Puerto Rico’s economic growth. Understanding Act 60 is crucial for anyone considering a move for business or investment, as it profoundly shapes the financial landscape and the lifestyle opportunities available on the island. These incentives are not merely tax breaks; they represent a strategic governmental push to foster job creation, stimulate real estate development, and diversify the economic base beyond traditional tourism.

Attracting Businesses: The Export Services Act (Formerly Act 20)

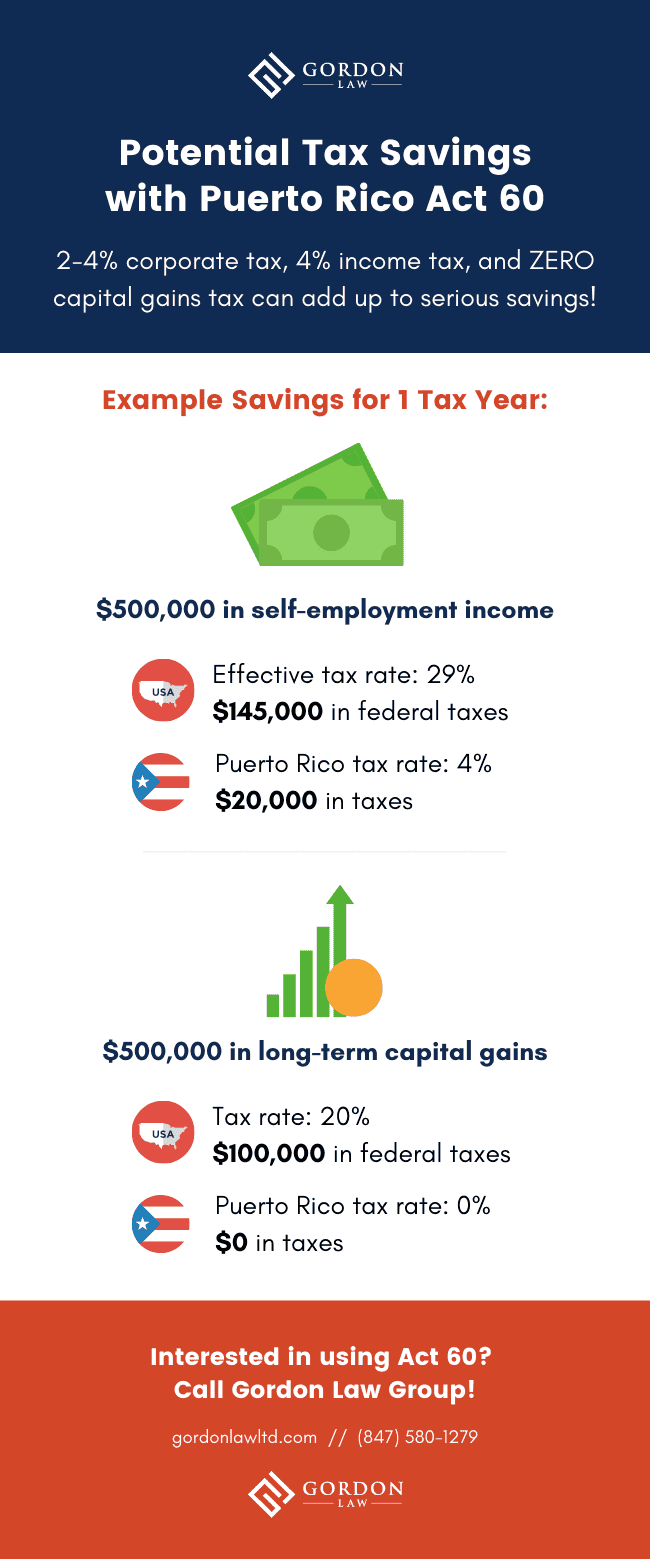

One of the cornerstones of Puerto Rico’s economic development strategy is the set of incentives aimed at export service companies, originally enacted as Act 20 and now integrated into Act 60. This provision offers an exceptionally low corporate tax rate of just 4% on eligible income derived from services rendered from Puerto Rico to clients outside the island. Furthermore, qualifying businesses can enjoy a 100% exemption on dividends distributed from earnings and profits generated under the incentive. This makes Puerto Rico an attractive hub for a wide array of service industries, including consulting, advertising, engineering, software development, call centers, and even financial services.

For entrepreneurs and businesses, the draw is clear: a dramatically reduced tax burden can significantly enhance profitability and enable greater reinvestment into growth. This influx of businesses contributes to the local economy by creating jobs, demanding professional services, and spurring innovation. From a tourism and lifestyle perspective, the growth of these sectors can lead to a more cosmopolitan environment, with a greater variety of high-quality hotels, diverse culinary experiences in cities like San Juan, and an overall enhancement of urban infrastructure and amenities. The presence of a thriving business community can also increase the demand for various accommodation types, from short-term rentals for business travelers to long-term stays for relocating employees.

For Individual Investors: The Individual Investors Act (Formerly Act 22)

Complementing the business incentives, Act 60 also incorporates provisions designed to attract individual investors and high-net-worth individuals, previously known as Act 22. This incentive offers a 100% tax exemption on all passive income – including interest, dividends, and short-term and long-term capital gains – accrued after becoming a bona fide resident of Puerto Rico. For individuals with substantial investment portfolios, this can translate into significant tax savings, potentially allowing them to retain a much larger portion of their investment returns than they would in the mainland U.S.

The appeal of this exemption is transformative for many, enabling them to reinvest more aggressively or simply enjoy a higher net income. This has led to an influx of affluent residents, particularly in desirable areas, which in turn influences the luxury travel and accommodation markets. We see a rise in high-end real estate developments, exclusive resorts, and sophisticated dining experiences, all catering to a clientele seeking both financial advantage and an elevated lifestyle. However, it’s crucial to understand that qualifying for these incentives is not automatic. It requires a genuine commitment to Puerto Rico as one’s primary home and a strict adherence to the residency requirements stipulated by the law. This incentive shapes a particular lifestyle niche, attracting those who value both financial prudence and the vibrant culture and natural beauty that Puerto Rico offers.

Defining “Bona Fide Resident”: Eligibility for Incentives

The cornerstone of eligibility for Puerto Rico’s tax incentives, particularly for individuals seeking the benefits of the former Act 22 (now part of Act 60), is becoming a “bona fide resident” of the island. This isn’t just about spending a few weeks on vacation; it’s a legal designation with specific criteria that must be met to satisfy both Puerto Rico and U.S. federal tax authorities. The IRS outlines three key tests to determine bona fide residency:

- Presence Test: An individual must generally be present in Puerto Rico for at least 183 days during the taxable year. This means physically residing on the island for more than half the year, a significant commitment that goes beyond typical travel or extended stays.

- Tax Home Test: The individual’s tax home must be in Puerto Rico. A “tax home” refers to the general area of an individual’s main place of business, employment, or post of duty, regardless of where they maintain a family home. If there is no regular or principal place of business, the tax home is the place where the individual regularly lives. This implies a genuine economic connection to the island.

- Closer Connection Test: The individual must not have a “closer connection” to the United States or a foreign country than to Puerto Rico. This is a qualitative test, looking at a variety of factors to determine where an individual’s true center of life lies. Factors considered include the location of the individual’s permanent home, family, personal belongings, social, political, cultural, or religious affiliations, business activities, and driver’s license issuance. This requires tangible actions to integrate into the Puerto Rican community, such as enrolling children in local schools, joining local organizations, or establishing a primary residence.

Meeting these stringent requirements demonstrates a genuine intent to integrate into Puerto Rico’s society and economy, rather than simply leveraging its tax benefits without contributing to the local fabric. For those considering relocation, understanding these tests is critical for planning not just their finances but also their lifestyle, accommodation choices, and overall engagement with the island. It underscores that enjoying the tax benefits requires a true commitment to making Puerto Rico home, fostering a deeper connection to its local culture and community.

Beyond the Incentives: Practical Tax Considerations for Residents and Visitors

While the high-profile tax incentives often dominate discussions about Puerto Rico’s fiscal environment, it’s essential to consider the broader practical implications for both long-term residents and transient visitors. The island’s tax structure, while unique, impacts daily life, the cost of living, and the overall economic vitality that contributes to its appeal as a travel destination. Understanding these everyday tax realities provides a more holistic view beyond the specific benefits for qualified investors and businesses.

Daily Life and Local Taxation

For anyone living, working, or simply enjoying an extended stay in Puerto Rico, local taxes are an inescapable part of daily life. The primary revenue generator at the local level is the sales and use tax, known as IVU (Impuesto sobre Ventas y Uso). While the precise rate can fluctuate, it is applied to most goods and services, similar to sales taxes in the U.S. states. This directly affects the cost of groceries, restaurant meals, retail purchases, and even hotel stays, impacting both budget-conscious travelers and those enjoying luxury experiences. For example, a stay at a resort in Dorado or a boutique hotel in Old San Juan will include this tax, just as dining at a local eatery or buying souvenirs will.

Beyond sales tax, property taxes are levied on real estate, a crucial factor for those considering purchasing a home or investing in long-term accommodation. These taxes contribute to local municipal services and infrastructure, which in turn affect the quality of life and the attractiveness of different neighborhoods for residents and potential visitors. Excise taxes on certain goods, such as fuel, alcohol, and tobacco, also contribute to the local economy and influence consumer prices. Understanding these various local levies is fundamental to budgeting for life in Puerto Rico, allowing individuals to accurately assess their cost of living and plan their expenditures, whether for a temporary visit or a permanent move. This intricate web of local taxes underpins the public services and infrastructure that make Puerto Rico a functioning and appealing destination.

The Broader Economic and Lifestyle Impact

The interplay of federal tax exemptions and local tax incentives has a profound ripple effect on Puerto Rico’s economy and, consequently, on the lifestyle it offers. The incentives, by attracting new businesses and affluent individuals, stimulate economic activity, leading to job creation in various sectors. This economic injection contributes to improvements in infrastructure, the development of new housing (including upscale options for the new demographic), and an expansion of services, from healthcare to entertainment. The rising demand for luxury accommodations and services, for example, has spurred the development of high-end resorts and private villas, diversifying Puerto Rico’s tourism offerings.

This economic growth also means more vibrant cultural scenes, a wider array of culinary experiences, and enhanced recreational opportunities. For travelers, this translates into a richer and more varied experience, with modern amenities blending seamlessly with Puerto Rico’s rich history and natural beauty. However, the economic changes are not without their complexities. Increased demand for housing and services can lead to rising costs, which can be a concern for long-standing local residents and for budget travelers. The challenge for Puerto Rico lies in balancing the economic benefits of its tax policies with ensuring equitable development and preserving its unique cultural identity for all. Ultimately, the tax structure is a key driver in shaping modern Puerto Rico, influencing everything from its bustling urban centers to its tranquil coastal towns, and providing a dynamic backdrop for travel, accommodation, and diverse lifestyles.

Puerto Rico’s Fiscal Future: Debates and Dynamics

The unique tax landscape of Puerto Rico, particularly its incentive programs, has not been without scrutiny and ongoing debate. While undoubtedly successful in attracting investment and talent, these policies also raise important questions about equity, long-term sustainability, and the island’s economic identity. Understanding these dynamics is crucial for appreciating the full context of Puerto Rico’s tax situation and its potential future trajectory, especially for those considering a significant commitment to the island.

Addressing the “Tax Haven” Narrative

One of the most frequent criticisms or discussions surrounding Puerto Rico’s tax incentives, particularly Act 60’s provisions for individual investors (formerly Act 22), is the perception that it operates as a “tax haven.” Proponents of the incentives argue that this label is misleading, emphasizing that the laws are designed for genuine economic development and require bona fide residency and contributions to the local economy. They highlight the rigorous residency requirements and the fact that individuals and businesses are still subject to significant local taxes, Social Security, and Medicare contributions. The goal is to encourage permanent relocation and business establishment, fostering job growth and capital injection into the island, rather than simply providing a loophole for passive income.

However, critics often point to the stark contrast between the zero-tax rate on passive income for new residents and the tax burdens faced by long-term local residents, raising questions of fairness and economic disparity. There is an ongoing dialogue about the extent to which these incentives truly benefit the broader Puerto Rican populace versus primarily enriching a select group of newcomers. This narrative impacts Puerto Rico’s international image and influences discussions about its economic future, including its relationship with the U.S. federal government. For individuals exploring a move or investment, understanding these complex viewpoints is important for making an informed decision and for engaging responsibly with the local community and economy.

The Ongoing Evolution of Tax Policy

The tax policies in Puerto Rico are not static; they are subject to ongoing review, modification, and adaptation. The consolidation of previous laws (Act 20 and Act 22) into Act 60 is a prime example of this evolution, reflecting the government’s efforts to streamline processes, address criticisms, and ensure the programs remain effective and aligned with current economic goals. The debates surrounding economic development, fiscal responsibility, and social equity continue to shape legislative discussions on the island.

Furthermore, Puerto Rico’s fiscal relationship with the United States is a dynamic one, influenced by broader federal policy, economic shifts, and the ongoing dialogue about the island’s political status. Potential changes to federal tax laws or a shift in Puerto Rico’s territorial status could significantly alter the current tax landscape. Therefore, for anyone deeply invested in Puerto Rico, whether as a resident, business owner, or long-term visitor, staying informed about these policy developments is crucial. Navigating this evolving environment requires diligence and often the guidance of local tax professionals who can provide up-to-date advice. This dynamic fiscal environment underpins the island’s journey towards economic stability and prosperity, continuously influencing the attractiveness of its hotels, the vibrancy of its tourism sector, and the unique lifestyle it offers.

In conclusion, the question “Does Puerto Rico pay taxes?” opens a window into a fascinating and intricate fiscal world. While its residents enjoy a unique exemption from federal income tax on Puerto Rico-sourced income, they contribute significantly through local taxes and federal social programs. The strategic tax incentives, particularly under Act 60, have played a pivotal role in shaping Puerto Rico’s economic resurgence, attracting a new wave of businesses and individuals who contribute to the island’s vibrant culture, diverse accommodation options, and evolving lifestyle. As Puerto Rico continues to evolve, its distinct tax policies will remain a central pillar of its identity and its ongoing efforts to build a resilient and prosperous future.