The allure of a new destination, the comfort of a well-appointed hotel suite, or the thrill of exploring local culture in a vibrant city like Paris or Rome is undeniable. As we embark on journeys for leisure, business, or family trips, our focus is often on the experiences ahead: the attractions, the cuisine, and the memories we’ll create. However, a crucial but often overlooked aspect of travel planning is understanding how our existing insurance policies protect us when we’re away from home. One common question that frequently arises among individuals renting their primary residence is: “Does renters insurance cover hotel stays?”

This isn’t just a hypothetical query; it touches upon the very practical concerns of safeguarding our belongings and financial well-being during our travels. Whether you’re staying at a boutique hotel in London, a sprawling resort in Cancun, or even a short-term apartment through platforms like Airbnb, understanding the nuances of your renters insurance policy is paramount. While renters insurance is primarily designed to protect your personal property and provide liability coverage within your rented dwelling, its scope can sometimes extend to situations outside your home, including your temporary accommodation. However, the extent of this coverage is often limited and specific, making it essential to delve into the details. This guide will explore the various facets of renters insurance, its potential applicability to hotel stays, its limitations, and alternative protections to ensure your peace of mind while exploring the world.

Understanding Renters Insurance Basics

Before we can ascertain whether your renters insurance extends to your hotel stays, it’s vital to have a clear understanding of what a standard policy typically covers. Renters insurance is a financial safety net designed for individuals who rent their homes, whether that’s an apartment, a house, or even a dorm room. Unlike homeowner’s insurance, it does not cover the structure of the building itself, as that is the responsibility of the landlord. Instead, it focuses on protecting the tenant’s personal assets and liabilities.

What Renters Insurance Typically Covers

A typical renters insurance policy is comprised of three main components:

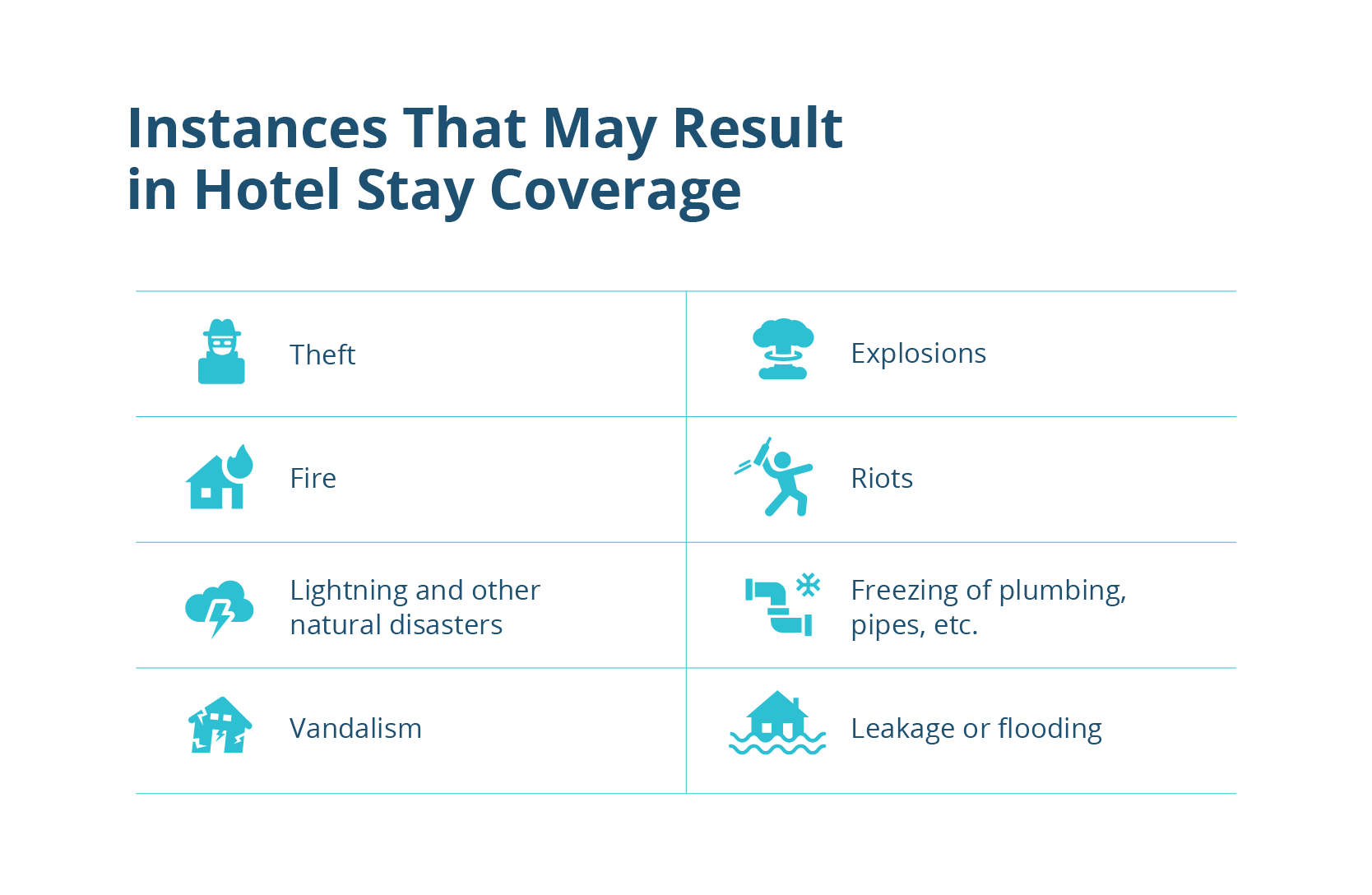

- Personal Property Coverage: This is perhaps the most relevant component when discussing hotel stays. It protects your personal belongings from specified perils, such as fire, theft, vandalism, smoke, and certain types of water damage. This includes everything from your furniture and electronics to clothing and jewelry. When a covered event occurs, your insurer will help replace or repair these items, up to your policy’s limits and after your deductible has been met. For instance, if a fire breaks out in your apartment and damages your possessions, this coverage would kick in.

- Personal Liability Coverage: This component protects you financially if you are found legally responsible for causing bodily injury to another person or for damaging their property, whether at your rental unit or elsewhere. For example, if a guest slips and falls in your apartment and sues you, your liability coverage would help cover their medical bills and your legal defense costs. This can also extend to situations where you accidentally damage someone else’s property, like knocking over an expensive vase at a friend’s house.

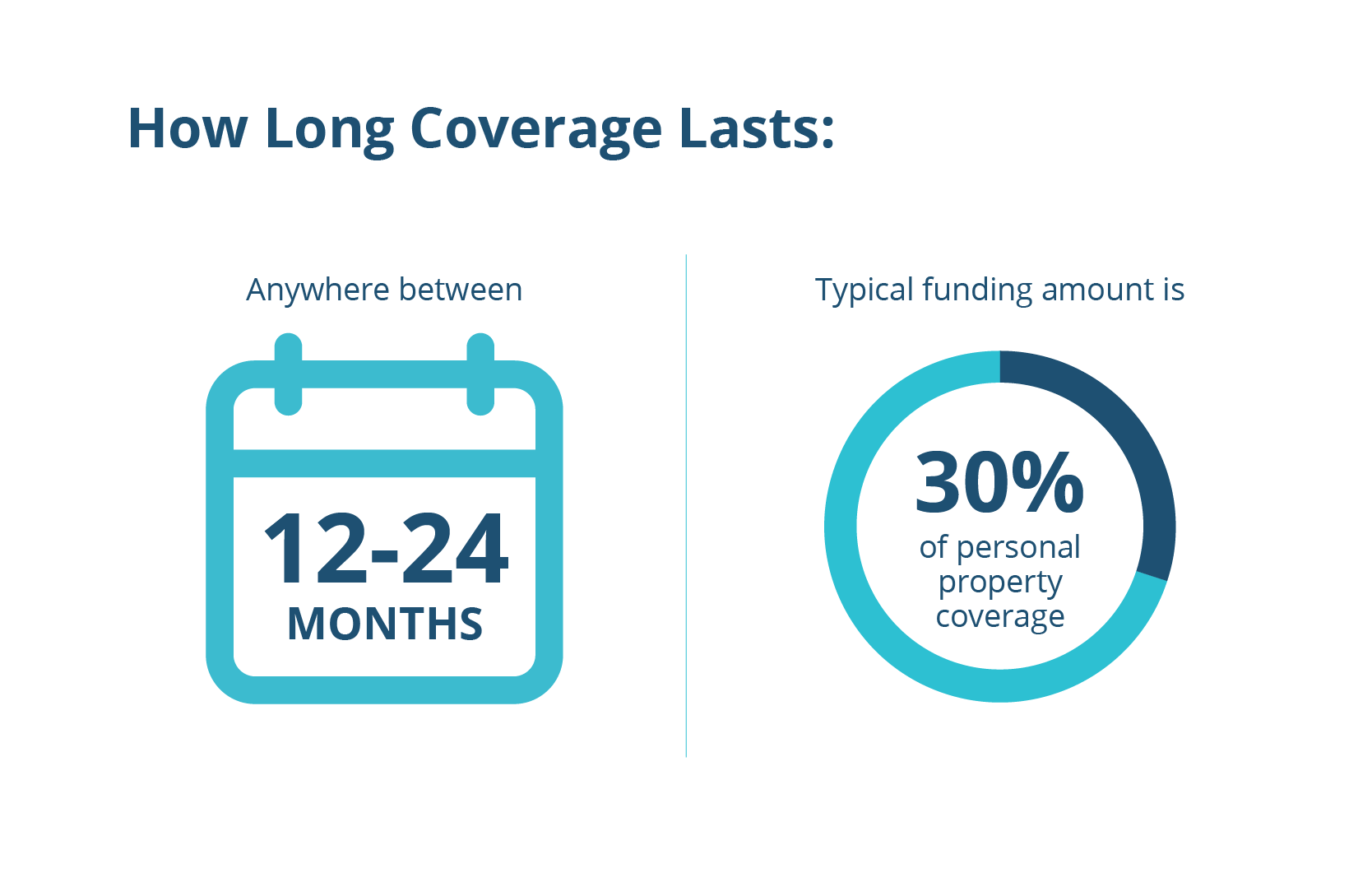

- Additional Living Expenses (ALE) or Loss of Use Coverage: Also known as ALE, this coverage helps pay for temporary housing and other living expenses if your rented home becomes uninhabitable due to a covered peril. For instance, if a severe storm damages your apartment building and you need to relocate while repairs are made, your policy might cover the cost of a hotel or temporary rental, as well as increased food costs, up to a certain limit and for a specified period. This is distinctly different from simply choosing to stay in a hotel for travel.

The ‘Off-Premises’ Clause: A Key to Travel Coverage

Crucially, the personal property component of many renters insurance policies includes an “off-premises” clause. This provision states that your personal belongings are covered not just within the confines of your rental unit, but also when they are with you anywhere else in the world. This is the cornerstone of how renters insurance might extend to your hotel stays.

While the exact percentage varies by insurer and policy, it’s common for policies to offer 10% to 50% of your total personal property coverage amount for items stolen or damaged away from your primary residence. So, if you have $30,000 in personal property coverage, you might have between $3,000 and $15,000 in coverage for items stolen from your hotel room in New York City or while sightseeing at the Eiffel Tower in France. However, this reduced limit is a significant factor to consider, especially if you travel with valuable items. It’s essential to consult your specific policy documents or speak with your insurance provider, such as State Farm or GEICO, to understand the precise limits and conditions of your off-premises coverage.

When Your Renters Insurance Might Cover Hotel Stays

Given the “off-premises” coverage, renters insurance can indeed offer a layer of protection during your hotel stays, primarily for the theft or damage of your personal belongings. It’s not a comprehensive travel insurance policy, but it can provide a useful safety net under specific circumstances.

Theft of Personal Property

This is the most common scenario where your renters insurance might come into play while you’re traveling. If your luggage, laptop, jewelry, or other personal items are stolen from your hotel room, a common area within the hotel like the lobby of a Grand Hyatt, or even from a secured rental car parked outside, your personal property coverage could provide reimbursement. This also extends to items stolen from your person while you’re out exploring tourist attractions, for example, a camera snatched while you’re admiring the Colosseum in Italy or a wallet lifted in a crowded market.

To file a successful claim for theft, you will almost certainly need a police report from the location where the theft occurred. This documentation is crucial for your insurer to process the claim. Remember, the coverage will be subject to your policy’s deductible and the off-premises coverage limits, which, as mentioned, are usually lower than your at-home coverage. If your deductible is high, say $500, and the stolen item is worth $700, you might only receive $200 from your insurer, making small claims less impactful.

Damage to Personal Property

While less frequent in a hotel setting compared to theft, your personal property coverage could also extend to damage sustained by your belongings while you’re away from your primary residence. For instance, if your suitcase and its contents are damaged during an airline’s handling on the way to a luxury resort, or if your laptop is damaged in a hotel fire, your renters insurance could potentially cover the cost of repair or replacement. However, it’s important to note that “accidental damage” where you are at fault (e.g., you spill coffee on your own laptop) is often not covered unless you have an “open perils” policy or a specific endorsement for such events. Most renters insurance policies are “named perils,” meaning they only cover damage from events specifically listed in the policy.

Personal Liability (Very Specific Cases)

While the primary function of personal liability coverage is for incidents within your home or general interactions, there are niche scenarios where it might indirectly apply to a hotel stay. If, for example, you accidentally cause significant damage to the hotel property that goes beyond normal wear and tear and the hotel subsequently holds you responsible for the repair costs, your personal liability coverage might offer some protection. An extreme example could be if you negligently cause a sprinkler system to activate, flooding several hotel rooms. However, this is quite rare, as most hotels have their own property insurance to cover damage to their structure and amenities. Moreover, liability coverage is more commonly invoked when you injure another person or damage their property, not the property of the establishment you are staying in. It’s crucial not to confuse this with the hotel’s own insurance which would cover most accidental damage to their premises.

Limitations and Exclusions: When Renters Insurance Falls Short

Despite the potential for off-premises coverage, it’s critical to understand that renters insurance is not a substitute for dedicated travel insurance. There are significant limitations and exclusions that often mean your policy will fall short of providing comprehensive protection during your travels.

High-Value Items and Sub-Limits

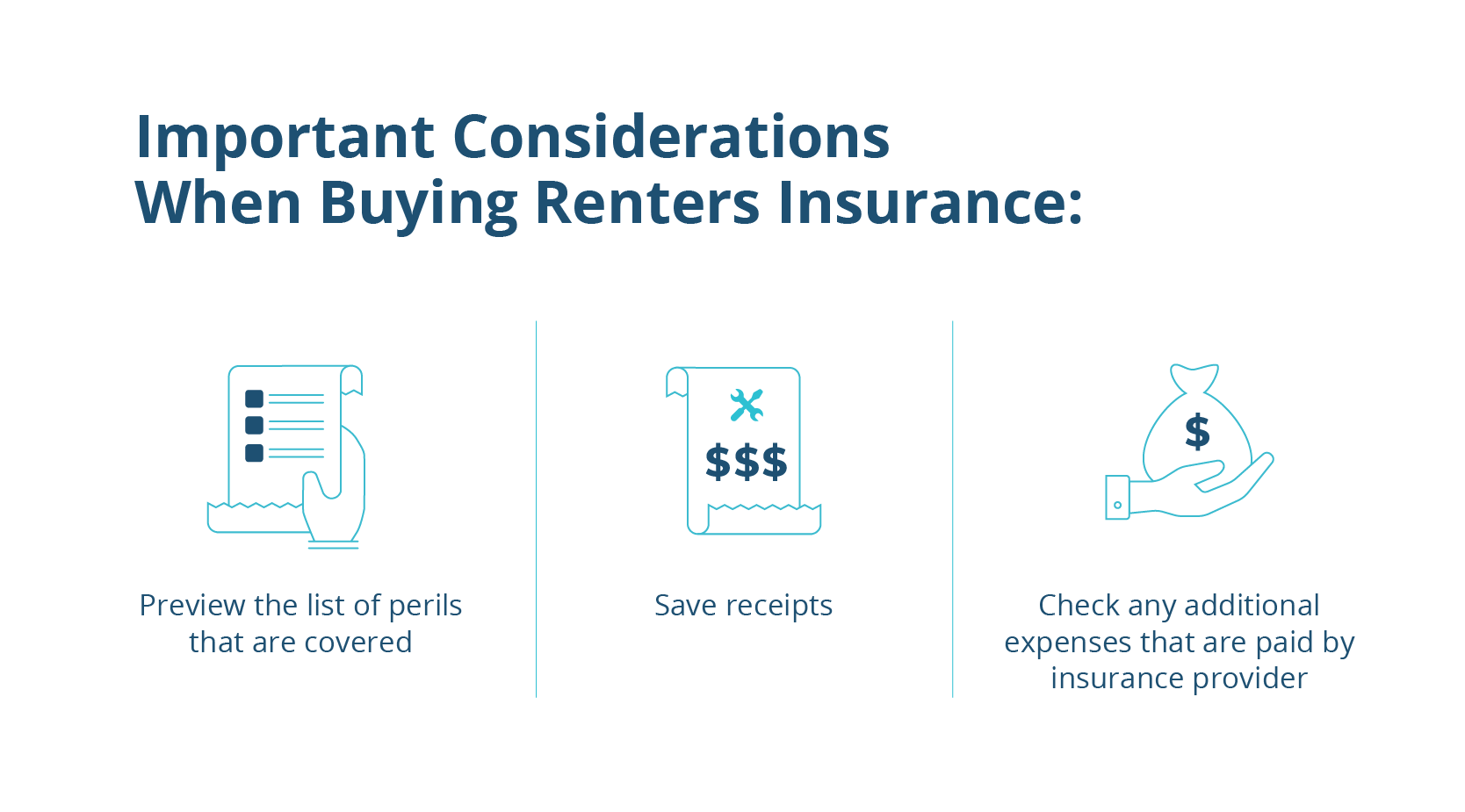

Many renters insurance policies impose “sub-limits” on certain categories of high-value items, regardless of your overall personal property coverage limit. Jewelry, furs, fine art, collectibles, firearms, and even expensive electronics often have specific, lower limits for theft or loss. For example, your policy might cover up to $2,500 for jewelry theft, even if your total personal property coverage is $50,000. If you travel with a diamond necklace worth $10,000 that gets stolen from your hotel safe in Dubai, your renters insurance would only reimburse you up to the sub-limit, leaving a substantial gap.

For such items, you would typically need to purchase a “scheduled personal property endorsement” (also known as a “floater”). This add-on allows you to insure specific high-value items individually for their appraised value, often covering a broader range of perils and without a deductible. Without such an endorsement, traveling with expensive watches bought in Zurich or designer handbags could leave you significantly underinsured.

Damage to the Hotel Property and Rental Cars

As mentioned, renters insurance is not designed to cover damage to the structure or furnishings of the hotel itself. If you accidentally spill wine on the carpet, break a lamp, or damage a TV screen in your hotel room, the hotel’s property insurance will likely cover the repairs. They may, however, charge you directly for the damages. Your renters liability might come into play if the damage is severe and you are legally held responsible, but it’s not a primary go-to for typical hotel damages.

Similarly, renters insurance almost never covers damage to a rental car. For this, you would typically rely on your personal auto insurance policy (if it extends coverage to rentals), coverage offered by the rental car company (often expensive), or benefits provided by certain credit cards like Chase Sapphire Reserve or American Express Platinum if you used them to book the rental.

Loss of Use/Accommodation Costs (Travel-Related)

A common misconception is that if a trip is unexpectedly cut short or you need to extend your stay due to an unforeseen event, renters insurance will cover the additional hotel costs. This is generally not true. The Additional Living Expenses (ALE) coverage in your renters policy is specifically tied to your primary residence becoming uninhabitable due to a covered peril. It does not cover the cost of hotel stays simply because your travel plans change, you miss a flight, or you face other travel-related inconveniences. For example, if you’re stranded in Miami due to a flight cancellation, your renters insurance won’t pay for your extra nights at a Hilton hotel.

Mysterious Disappearance and Non-Covered Perils

If an item simply goes missing without any evidence of theft (e.g., it wasn’t stolen from a locked hotel room but you simply can’t find it), most renters insurance policies will classify this as “mysterious disappearance” and will not cover the loss. There needs to be clear evidence of a covered peril, such as a police report for theft or a fire report for damage, to trigger coverage. Furthermore, renters policies are “named perils” policies, meaning they only cover risks specifically listed. Exclusions might include acts of war, nuclear hazard, government action, or certain types of natural disasters depending on your specific policy and location.

Alternatives and Supplements to Renters Insurance for Travel

Given the limitations of renters insurance for travel, it’s clear that relying solely on it for protection during your hotel stays and journeys is insufficient. Fortunately, several dedicated alternatives and supplements offer more comprehensive coverage.

Travel Insurance

This is the gold standard for protecting your investment in a trip and your well-being while traveling. Travel insurance policies are specifically designed to cover a wide range of travel-related risks that renters insurance simply doesn’t touch. Key coverages typically include:

- Trip Cancellation/Interruption: Reimburses non-refundable expenses if you have to cancel or cut short your trip due to covered reasons (e.g., illness, family emergency, natural disaster).

- Medical Emergencies: Covers emergency medical treatment, hospitalization, and sometimes even emergency medical evacuation, which is crucial when traveling internationally, especially to places like Thailand where medical costs can be high.

- Lost or Delayed Baggage: Provides reimbursement for essential items if your luggage is delayed, and covers the value of lost luggage up to a certain limit, often more generously than renters insurance.

- Travel Delay: Reimburses for expenses like extra hotel nights or meals if your trip is delayed for a specified period (e.g., 6+ hours).

- Rental Car Coverage: Many policies offer optional collision damage waiver for rental cars.

You can purchase single-trip policies for specific journeys or annual multi-trip policies if you travel frequently. Reputable providers like Allianz Travel Insurance or World Nomads offer various plans.

Credit Card Benefits

Many premium travel credit cards, such as the Visa or Mastercard variants designed for travelers, offer a surprising array of built-in travel insurance benefits, provided you pay for your trip with that card. These can include:

- Rental Car Collision Damage Waiver (CDW): Often secondary, meaning it kicks in after your personal auto insurance, but some are primary.

- Lost or Delayed Baggage Coverage: Supplements or replaces airline compensation.

- Trip Delay/Cancellation Coverage: For covered reasons.

- Emergency Medical Evacuation: In severe cases.

Always read your credit card’s guide to benefits carefully, as terms and conditions can be complex, and coverage amounts vary widely. These benefits can significantly enhance your protection without additional cost.

Homeowners Insurance

For those who own their homes, homeowners insurance operates on a similar principle to renters insurance regarding personal property. Most homeowners policies also include an “off-premises” clause, meaning your belongings are protected worldwide, subject to similar limitations, deductibles, and sub-limits for high-value items. Homeowners might find their off-premises coverage slightly more generous than renters policies, but the fundamental limitations for travel remain.

Valuables Riders/Endorsements

As discussed earlier, for specific high-value items like engagement rings, professional photography equipment, or antique watches, a scheduled personal property endorsement added to your renters or homeowners policy is almost always the best option. These endorsements provide broader coverage, often including “mysterious disappearance,” and insure the item for its appraised value, typically without a deductible. This ensures that a cherished piece of jewelry is adequately protected whether it’s safely at home or being worn during a special dinner at a Four Seasons hotel.

Practical Tips for Protecting Your Belongings While Traveling

Beyond insurance, proactive measures are your first line of defense against loss or damage during your hotel stays and travels.

Inventory and Documentation

Before you even leave your home, create a detailed inventory of the valuables you plan to take with you. Take photos or videos of these items, especially electronics and jewelry, noting their condition. Keep a record of serial numbers for all electronic devices. This documentation is invaluable if you need to file an insurance claim, providing concrete evidence of what was lost or damaged. Store copies of this inventory (and your policy details) digitally and in a separate location from your physical belongings.

Smart Packing and Storage

Be strategic about what you bring and how you store it. Avoid packing irreplaceable or extremely valuable items in checked luggage; always carry them on. Utilize hotel safes for passports, extra cash, and small valuables when you’re out exploring. When leaving your hotel room, ensure windows are closed and doors are locked. In some cases, if you’re staying at an apartment or villa for an extended period, treat it like your home, locking up diligently.

Consider using secure travel bags or backpacks, especially in crowded tourist areas like Times Square in New York City or bustling markets in Tokyo. Don’t leave bags unattended, even for a moment, and be wary of pickpockets, particularly in areas known for them.

Awareness and Vigilance

Common sense goes a long way. Be aware of your surroundings, especially when carrying bags, using your phone, or withdrawing cash from an ATM. Avoid openly displaying expensive jewelry or electronics that might attract unwanted attention. Research common scams or safety concerns in your destination, whether it’s the bustling streets of Sydney or a quiet village in the United States. Trust your instincts; if a situation feels unsafe, remove yourself from it.

Review Your Policy Before You Travel

The most important tip is to proactively review your existing renters insurance policy before any significant trip. Contact your insurance agent or company (e.g., Liberty Mutual or Progressive) and specifically ask about your off-premises personal property coverage limits, deductibles, and any exclusions that might apply to your travel plans. Discuss any high-value items you plan to bring and inquire about adding a scheduled personal property endorsement if needed. Understanding your coverage before you depart will prevent unpleasant surprises if an unfortunate incident occurs.

Conclusion

The question “Does renters insurance cover hotel stays?” has a nuanced answer: yes, to a limited extent, primarily for the theft or damage of personal property under the “off-premises” clause. While it can provide a valuable safety net for your belongings when you’re exploring destinations from the British Museum to Machu Picchu, it is by no means a comprehensive solution for travel protection.

Renters insurance typically does not cover trip cancellations, medical emergencies abroad, lost revenue from missed flights, or extensive damage to hotel property. For these broader travel risks, dedicated travel insurance, potentially supplemented by credit card benefits or specific endorsements for high-value items, is essential. Before your next adventure, whether it’s a relaxing beach vacation or an adventurous trek up Mount Everest or diving in the Great Barrier Reef, take the time to review your insurance policies. Understand their limitations, explore additional coverage options, and implement practical safety measures to ensure your peace of mind and protect your cherished belongings, allowing you to fully immerse yourself in the joys of travel and create unforgettable experiences.