The allure of new destinations, the comfort of a well-appointed hotel room, and the excitement of exploring unfamiliar attractions are central to the joy of travel. Whether planning a romantic getaway to Paris, a business stay in New York City, or a family trip to Orlando, the question of how your existing insurance protects you often arises. One common query that puzzles many travelers is whether their standard renters insurance policy extends its coverage to incidents that occur while staying in a hotel, resort, apartment, or even a villa abroad. This is a critical point of understanding, as the peace of mind that comes from knowing your belongings and liabilities are covered can significantly enhance your travel experience.

Renters insurance, primarily designed to protect your personal property and provide liability coverage within your rented dwelling, sometimes offers an unexpected degree of protection when you’re on the go. However, its scope is not limitless, and there are crucial distinctions between what renters insurance covers and what might require a dedicated travel insurance policy. Understanding these nuances is essential for any modern traveler, from the budget-conscious adventurer to the connoisseur of luxury travel. This comprehensive guide will delve into the specifics, helping you decipher the extent of your renters insurance coverage during your next journey.

Understanding the Reach of Your Renters Insurance Policy

At its core, renters insurance offers two primary categories of coverage: personal property and personal liability. The good news for travelers is that both of these often extend beyond the four walls of your primary residence, offering a safety net when you’re enjoying the local culture in Rome or exploring famous places like the Eiffel Tower. However, the devil is in the details, and the extent of this coverage can vary significantly based on your specific policy and the nature of the incident.

Personal Property Coverage: Your Belongings On The Go

One of the most valuable aspects of renters insurance for travelers is its personal property coverage. Most standard policies provide “off-premises” coverage, meaning your personal belongings are protected against covered perils, such as theft or fire, even when they are not inside your rented home. This protection typically extends worldwide, whether you’re vacationing in the Caribbean, hiking in the Swiss Alps, or attending a conference in London.

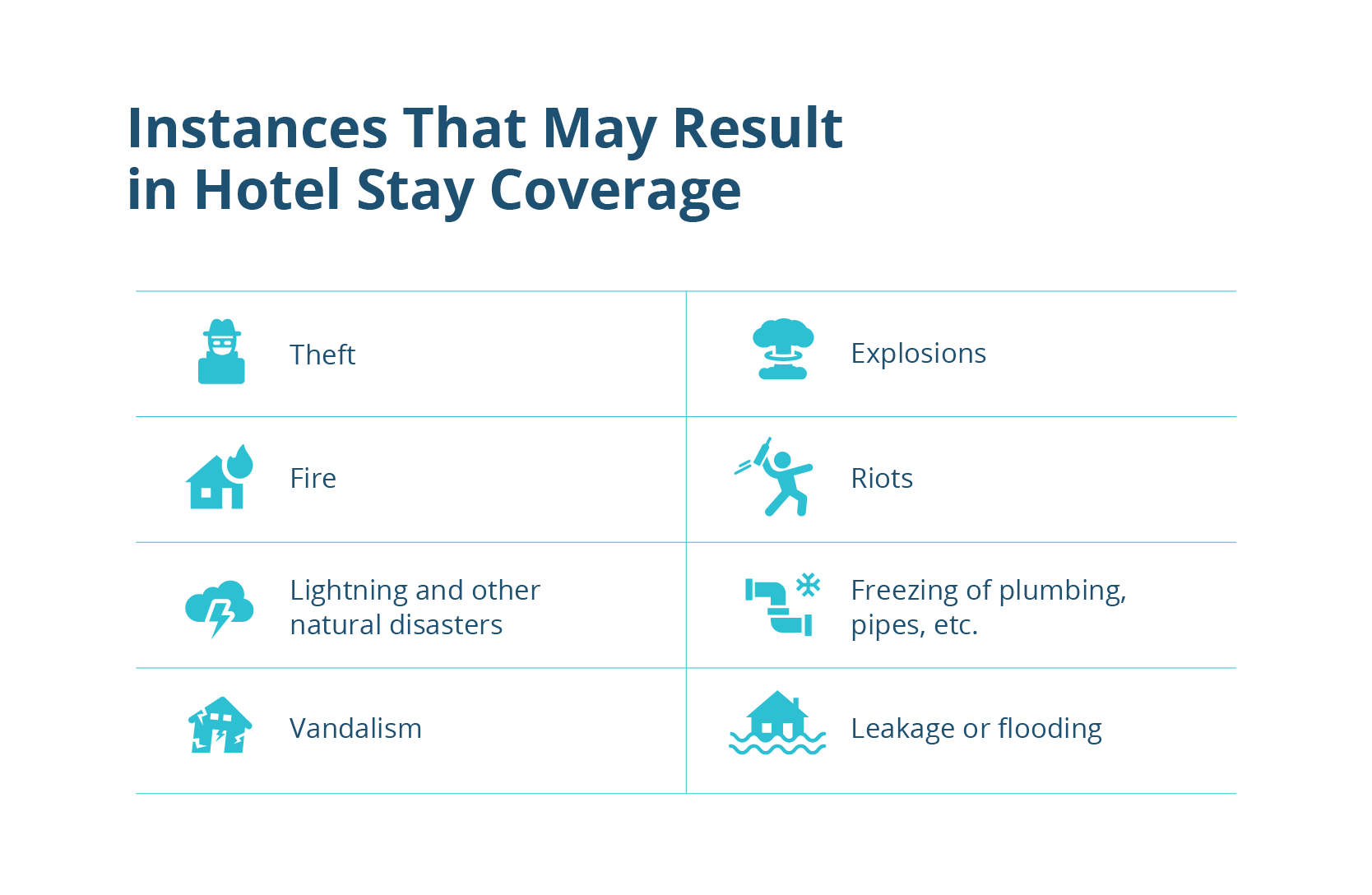

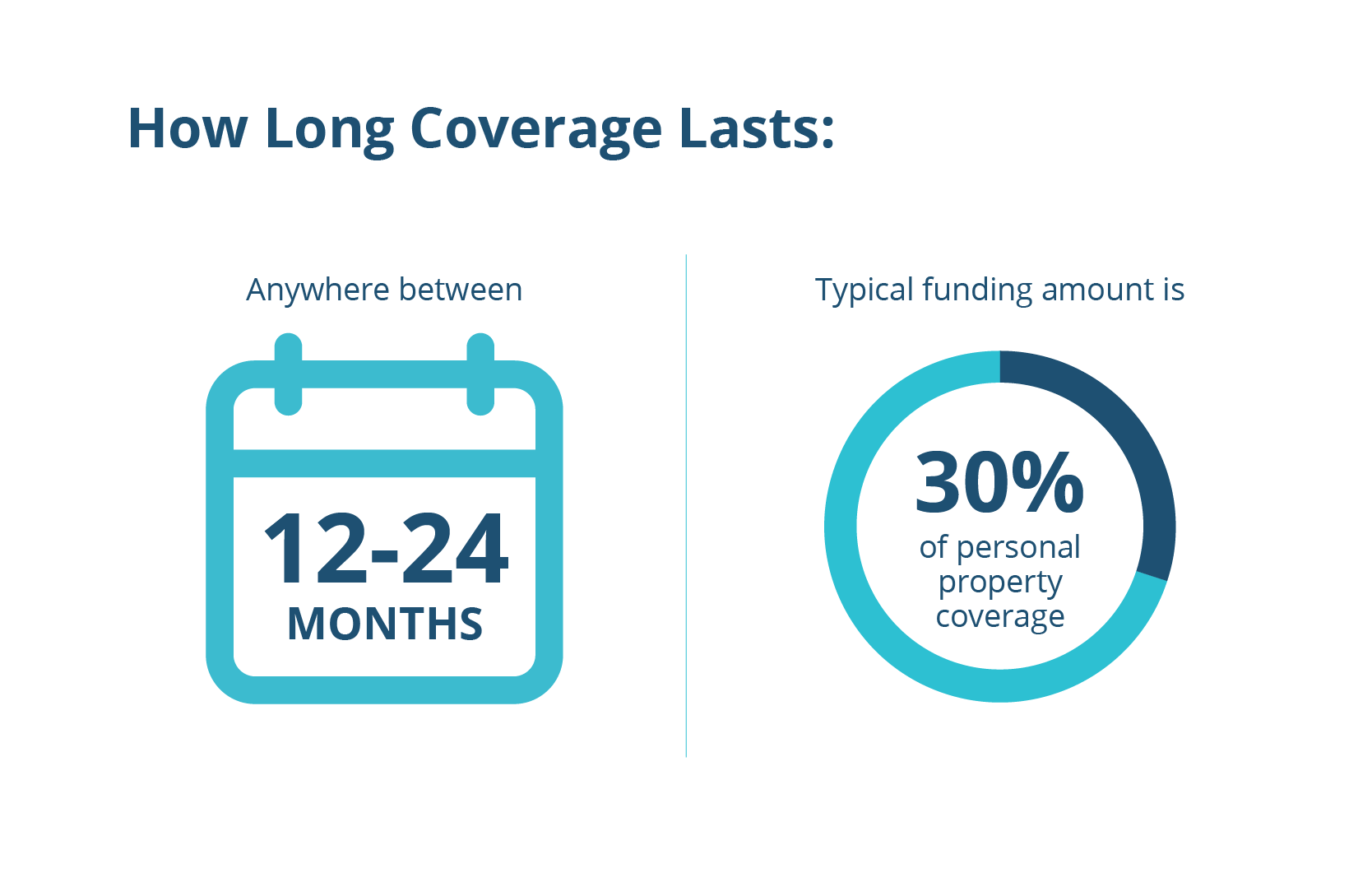

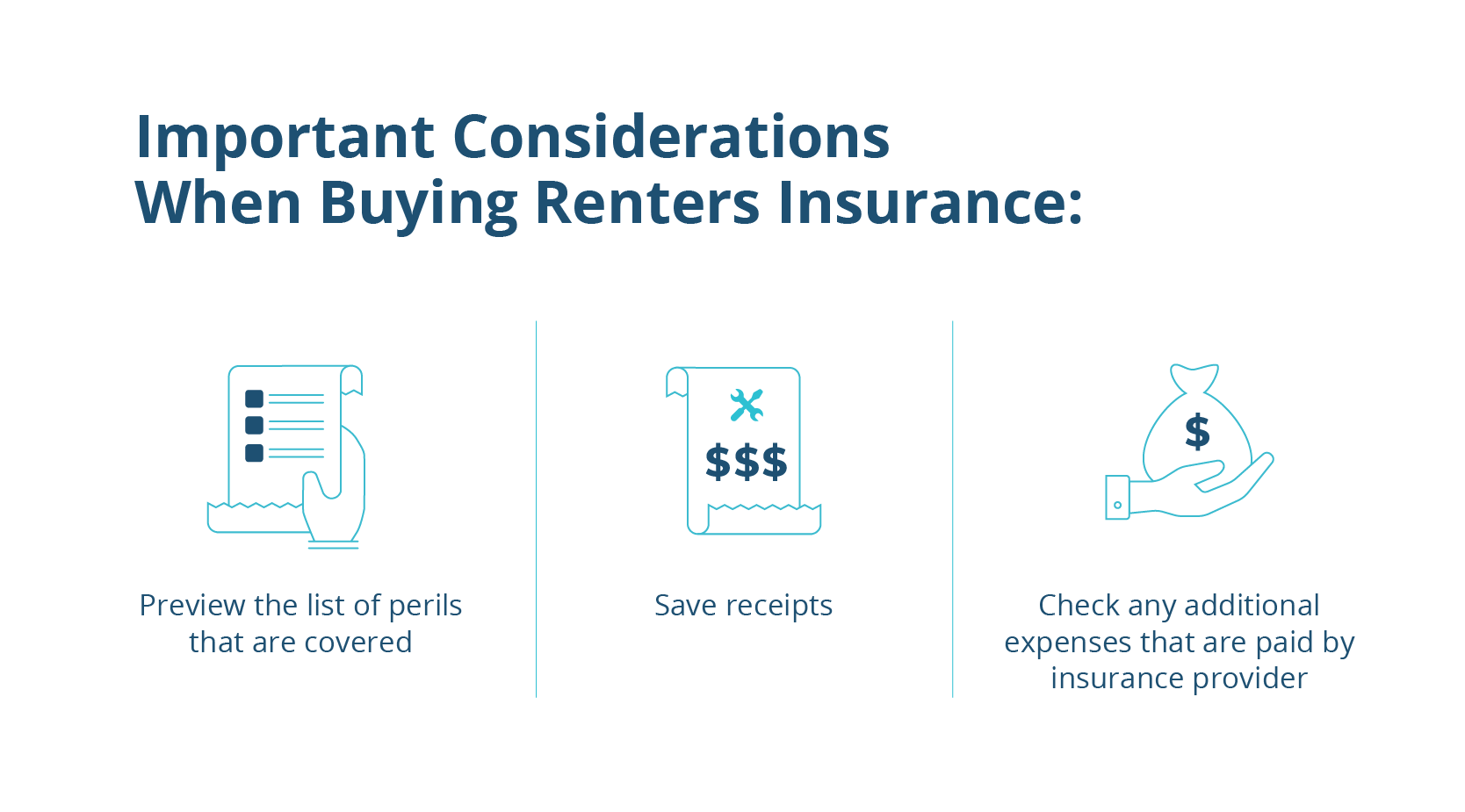

For instance, if your laptop, camera, or clothing is stolen from your hotel room at a Grand Hyatt Hotel or a quaint boutique hotel in Europe, your renters insurance policy may cover the loss. The key is that the loss must be due to a covered peril listed in your policy, such as theft, vandalism, or fire. It’s crucial to remember that this coverage usually comes with a deductible, which is the amount you must pay out-of-pocket before your insurance kicks in. Additionally, there are often sub-limits for certain high-value items like jewelry, electronics, or fine art, meaning your policy might only cover a fraction of their actual worth unless you have a specific rider or endorsement for these items. Therefore, it’s wise to review your policy documents or consult with your insurer before embarking on a trip with expensive valuables.

Personal Liability Coverage: Protection Beyond Your Walls

Beyond safeguarding your possessions, renters insurance also includes personal liability coverage, which is arguably even more critical for travelers. This portion of your policy protects you financially if you are held legally responsible for bodily injury to another person or damage to another person’s property, even when you’re away from home.

Imagine you’re staying at a Hilton resort in Hawaii and accidentally knock over an expensive vase in the lobby, or perhaps you cause a minor injury to another guest while engaging in a recreational activity. Your renters insurance liability coverage could potentially step in to cover the costs of damages or medical expenses, as well as any legal fees if you are sued. This protection extends globally, offering peace of mind whether you’re navigating the busy streets of Tokyo or enjoying a quiet retreat in rural France. However, deliberate acts are almost always excluded, and the coverage won’t protect the hotel property from your own negligence if it falls under your care (e.g., damaging your hotel room). For such incidents, the hotel typically handles minor damages, but for more significant issues, your liability coverage might become relevant.

Common Scenarios: When Renters Insurance Might (or Might Not) Apply in a Hotel

Navigating the specifics of insurance coverage during travel can be tricky. Let’s explore some common scenarios to clarify when your renters insurance might offer protection and when you’ll need to look elsewhere.

Theft of Personal Items

This is arguably the most common concern for travelers. If your camera bag is snatched from a café in Barcelona, or your luggage is stolen from your hotel room in Miami, your renters insurance’s personal property coverage typically extends to cover these losses, up to your policy limits and subject to your deductible. It’s crucial to report the theft to the local authorities and the hotel management immediately, as a police report is almost always required to file a claim. Documenting your belongings before your trip, perhaps with photos or a list of serial numbers, can also significantly streamline the claims process. This applies whether you’re staying at a budget hotel or a luxurious Marriott resort.

Accidental Damage to Hotel Property

What if you accidentally break a lamp in your hotel room or spill red wine on the pristine white carpet? While minor incidents are often handled directly by the hotel or charged to your credit card, for more significant damage, your renters insurance’s personal liability coverage could potentially apply. This coverage is designed to protect you from financial responsibility for damage you inadvertently cause to property that isn’t yours. However, some policies might have specific exclusions for property “in your care, custody, or control,” which could be argued to include your hotel room. Always review your policy and clarify with your insurer, especially if you are staying in high-end accommodations where potential damages could be substantial, such as a villa in Tuscany.

Medical Emergencies or Trip Cancellations

This is where a clear distinction between renters insurance and travel insurance becomes paramount. Renters insurance does not cover medical emergencies, emergency evacuations, trip cancellations, trip interruptions, or delays. If you fall ill during your vacation in Mexico and require hospitalization, or if unforeseen circumstances force you to cancel your meticulously planned cruise to Alaska, your renters policy will offer no financial assistance. These critical aspects of travel protection are exclusively covered by a dedicated travel insurance policy. For those embarking on international trips, especially to regions where medical costs are high, or for luxury travel where non-refundable deposits are substantial, travel insurance is an indispensable investment.

Natural Disasters and Specific Perils

If your personal belongings are damaged due to a natural disaster like a hurricane hitting your Florida resort or an earthquake in California, your renters insurance might cover the loss if that specific peril is covered by your policy. Most policies include coverage for common perils such as fire, smoke, windstorm, hail, and vandalism. However, floods and earthquakes are often excluded and require separate insurance policies or endorsements, even for your primary residence. When traveling, if your belongings are damaged by a covered peril while in your hotel room or other temporary accommodation, your personal property coverage would generally apply. Always check the specific perils listed in your policy.

Limitations and Exclusions: What Renters Insurance Won’t Cover at a Hotel

While renters insurance offers a helpful layer of protection, it’s vital to be aware of its inherent limitations and exclusions when you’re away from home. These carve-outs can significantly impact what you can claim and prevent disappointment during a stressful situation.

- High-Value Items and Sub-Limits: As mentioned, items like expensive jewelry, fine watches, furs, collectibles, and high-end electronics often have specific sub-limits within a standard renters insurance policy. This means that even if a $10,000 diamond necklace is stolen from your hotel safe in Zurich, your policy might only pay out $1,000 or $2,000 for jewelry unless you have added a “floater” or “endorsement” for that specific item. It’s always best to declare such items and purchase additional coverage if their value exceeds standard limits.

- Items Stolen from Unattended Vehicles: A common exclusion in many renters insurance policies is theft from an unattended vehicle. If your laptop bag is stolen from your rental car while it’s parked outside a restaurant in Seattle, your renters insurance might not cover the loss. Some policies may offer limited coverage for items stolen from a locked car, but this is not universal. This is a critical point for road trips and business travelers who often leave items in their vehicles.

- Cash: Renters insurance policies typically provide very limited, if any, coverage for lost or stolen cash. If a significant amount of currency is taken from your wallet or hotel room, you’re unlikely to be reimbursed by your renters policy. It’s always advisable to use credit cards when possible and limit the amount of cash you carry.

- Normal Wear and Tear or Accidental Loss: Renters insurance covers specific perils, not general wear and tear of your items or items that are simply lost (e.g., leaving your sunglasses on a beach in Bali and not being able to find them). For accidental loss, you might need a separate “scheduled personal property” endorsement or a comprehensive travel insurance policy that specifically includes “lost luggage” coverage.

- Damage to Your Rental Car: Renters insurance does not cover damage to your rental car. For this, you would rely on your personal auto insurance policy (if it extends to rental cars), the coverage offered by your credit card, or collision damage waiver (CDW) purchased from the rental car company.

- Business Inventory or Samples: If you’re traveling for business and carrying inventory, product samples, or equipment for your enterprise, these items are generally not covered by a standard renters insurance policy. You would typically need a separate business insurance policy for such protections.

- Intentional Acts: Damage to hotel property or injury to others caused by intentional acts are never covered by liability insurance. This protection is exclusively for accidental damage or negligence.

The Role of Travel Insurance: A Comprehensive Solution for Your Journeys

Given the limitations of renters insurance for travel-related risks, travel insurance emerges as a crucial and often indispensable solution for comprehensive protection. While renters insurance offers a valuable baseline for personal property and liability, it simply isn’t designed to address the multifaceted challenges unique to being away from home.

Travel insurance policies are specifically crafted to cover the diverse array of risks associated with trips, whether you’re embarking on an adventurous safari in Africa, a cultural exploration in Asia, or a scenic drive across North America. Key coverages typically include:

- Medical Emergencies and Evacuation: This is perhaps the most critical component, especially for international travel. If you fall ill or suffer an injury in South America, travel insurance can cover emergency medical treatments, hospital stays, and even medical evacuation back to your home country if necessary, which can cost tens of thousands of dollars out-of-pocket.

- Trip Cancellation and Interruption: If you have to cancel your trip before departure due to unforeseen circumstances (e.g., illness, job loss, natural disaster at your destination), travel insurance can reimburse your non-refundable expenses like flights and hotel bookings. If your trip is interrupted mid-journey, it can cover the costs of returning home early.

- Lost, Delayed, or Damaged Baggage: While renters insurance might cover stolen luggage, travel insurance often provides broader coverage for baggage that is lost by an airline, delayed, or damaged in transit. It can also offer reimbursement for essential items you need to purchase if your luggage is delayed for an extended period.

- Travel Delays: If your flight is significantly delayed, leading to missed connections or unexpected hotel stays, travel insurance can help cover additional expenses incurred.

- Adventure Activities: For those engaging in adventurous sports like skiing, scuba diving, or bungee jumping, some travel insurance policies offer specific riders for these higher-risk activities, which would be entirely outside the scope of renters insurance.

Considering the potential costs of medical emergencies abroad or the financial hit from a cancelled vacation, investing in travel insurance is a prudent decision for almost every traveler. It complements, rather than replaces, the limited coverage offered by renters insurance, providing a holistic safety net for your journeys, whether they involve luxury travel or a more budget-friendly exploration of Australia.

Practical Tips for Safeguarding Your Valuables While Traveling

While understanding insurance coverage is crucial, proactive measures can significantly reduce the risk of needing to file a claim in the first place. Smart packing and vigilant practices can make all the difference, enhancing your sense of security whether you’re staying at a bustling Grand Hyatt Hotel or a quiet guesthouse.

- Utilize Hotel Safes: Most hotels provide an in-room safe for valuables. While not impenetrable, these are generally a secure place to store passports, excess cash, jewelry, and small electronics when you’re out exploring the landmarks of London or the cultural attractions of Japan. Remember to use it for items you don’t need to carry with you daily.

- Keep Valuables Out of Sight: When leaving your hotel room, don’t leave expensive items like laptops, cameras, or tablets prominently displayed. Stow them away in a drawer, closet, or your closed luggage. In public areas, avoid flashing expensive gadgets or large sums of cash, especially in crowded tourist spots like Times Square or near the Statue of Liberty.

- Document Your Belongings: Before you leave home, take photos or videos of your valuable items. Note down serial numbers for electronics. This documentation will be invaluable if you need to file a police report or an insurance claim.

- Limit What You Carry: Consider leaving highly sentimental or extremely valuable items at home. Do you really need that heirloom diamond ring for your backpacking trip? The fewer valuables you bring, the less you have to worry about. This is especially true for budget travel.

- Be Aware of Your Surroundings: Whether you’re in a crowded market, on public transportation, or enjoying a meal outdoors, remain vigilant. Pickpockets often target distracted tourists. Keep bags zipped and in front of you, and consider an anti-theft bag for added security.

- Report Theft Immediately: If you experience a theft, report it to the hotel management and the local police as soon as possible. Obtain a copy of the police report, as this will be essential for any insurance claim.

- Secure Your Luggage: Use TSA-approved locks on your checked luggage. While these won’t deter a determined thief, they can prevent opportunistic theft. When traveling by bus or train, keep your carry-on luggage with you or within sight.

In conclusion, while your renters insurance policy does offer a baseline of protection for your personal property and liability when you’re away from your primary residence, including during hotel stays, it is not a comprehensive travel safety net. It can cover instances of theft of your belongings and certain liability claims, but it falls short in crucial areas such as medical emergencies, trip cancellations, or travel delays. For peace of mind and robust protection against the myriad of risks associated with travel, a dedicated travel insurance policy is highly recommended. Always review your renters insurance policy thoroughly before your trip and consider supplementing it with travel insurance to ensure all aspects of your journey are adequately covered, allowing you to focus on enjoying the experiences and making lasting memories.