[Florida], known as the Sunshine State, is a magnet for travelers seeking pristine beaches, vibrant cities, world-class theme parks, and a laid-back lifestyle. From the historic charm of [St. Augustine] to the exhilarating nightlife of [Miami] and the magical allure of [Orlando]’s attractions, [Florida] offers an unparalleled array of experiences. Whether you’re planning a short vacation, an extended stay, or contemplating a permanent move to embrace the [Florida] lifestyle, understanding the intricacies of car insurance is an essential part of your preparation. For many, a car is not just a convenience but a necessity for exploring the state’s diverse landscapes and enjoying its many offerings. However, navigating the world of car insurance in [Florida] can be complex, and its costs can significantly impact your travel budget or long-term living expenses. This comprehensive guide aims to demystify car insurance in [Florida], providing insights into average costs, mandatory coverages, factors influencing premiums, and strategies to secure the best rates, ensuring your [Florida] adventures are smooth and worry-free.

The Florida Driving Experience: Mandatory Coverage and Average Costs

Driving in [Florida] offers a unique blend of scenic routes and busy urban arteries. With millions of residents and tourists sharing its roads, understanding the state’s specific car insurance requirements is paramount. [Florida] operates under a “no-fault” insurance system, which significantly influences the types and amounts of coverage drivers are legally obligated to carry. This system is designed to streamline the process of medical claims after an accident, regardless of who caused it.

Unpacking Florida’s No-Fault System: PIP and PDL Explained

Under [Florida]’s no-fault law, drivers are required to carry Personal Injury Protection (PIP) insurance. This coverage pays for your medical expenses and, in some cases, lost wages, up to your policy limit, regardless of who was at fault in an accident. The minimum PIP coverage required in [Florida] is $10,000. This amount covers 80% of necessary medical expenses and 60% of lost wages, up to the policy limit. PIP is crucial for ensuring that you and your passengers receive prompt medical attention without the immediate need to determine fault. It’s a foundational element of ensuring peace of mind during your journeys, whether you’re navigating the bustling streets of [Tampa] or enjoying a scenic drive along the [Florida Keys].

In addition to PIP, [Florida] law also mandates Property Damage Liability (PDL) coverage. This insurance protects you if you cause damage to another person’s property, such as their vehicle, fences, or other structures, in an accident. The minimum PDL coverage required is $10,000. It’s important to note that while PIP covers your own injuries and PDL covers damage to other people’s property, neither of these mandated coverages addresses damage to your own vehicle or your liability for other people’s injuries. For comprehensive protection, especially when exploring popular tourist destinations or living in high-traffic areas, additional coverages are often highly recommended.

Average Premiums Across the Sunshine State: What to Expect

[Florida] generally has higher car insurance rates compared to the national average. Several factors contribute to this, including the high frequency of traffic accidents, a large number of uninsured drivers, a high incidence of insurance fraud, and the state’s susceptibility to severe weather events like hurricanes, which can lead to increased claims for vehicle damage. While national average car insurance rates hover around $1,700-$1,900 per year for full coverage, [Florida] residents can often expect to pay anywhere from $2,500 to over $4,000 annually, depending on a multitude of factors. Minimum coverage policies will, of course, be less expensive, but they offer significantly less financial protection.

These averages, however, are just starting points. The actual premium you pay will be highly individualized, varying significantly based on where you live within [Florida], your personal driving history, the type of vehicle you drive, and the specific insurance company you choose. For instance, drivers in metropolitan areas such as [Miami], [Orlando], and [Fort Lauderdale] typically face much higher rates than those in more suburban or rural locales like [Gainesville] or [Naples]. Understanding these baseline figures is crucial for anyone planning to integrate driving into their [Florida] experience, whether for daily commutes or leisurely trips to attractions like [Everglades National Park] or [Walt Disney World Resort].

Factors Shaping Your Florida Insurance Premium: From Miami to Orlando

The cost of car insurance in [Florida] is not a one-size-fits-all figure. Insurers use a complex algorithm of variables to assess risk and determine your premium. These factors range from personal demographics to geographical location and the specific coverages you select. Understanding these influences can empower you to make informed decisions and potentially lower your costs, leaving more room in your budget for [Florida]’s amazing experiences, from dining in [South Beach] to exploring the historic architecture of [Key West].

Your Profile and Your Ride: Personal Factors and Vehicle Impact

Several personal attributes play a significant role in how much you’ll pay for car insurance. Your age is a major factor, with younger, less experienced drivers (especially teenagers) often facing the highest rates due to a higher statistical likelihood of accidents. Rates tend to decrease as drivers gain experience and mature, typically plateauing in their 30s and 40s, before potentially rising again for senior drivers. Your driving record is arguably the most critical element; a history of accidents, traffic violations (like speeding tickets or DUIs), or numerous claims will almost certainly lead to higher premiums. Conversely, a clean driving record can unlock significant savings.

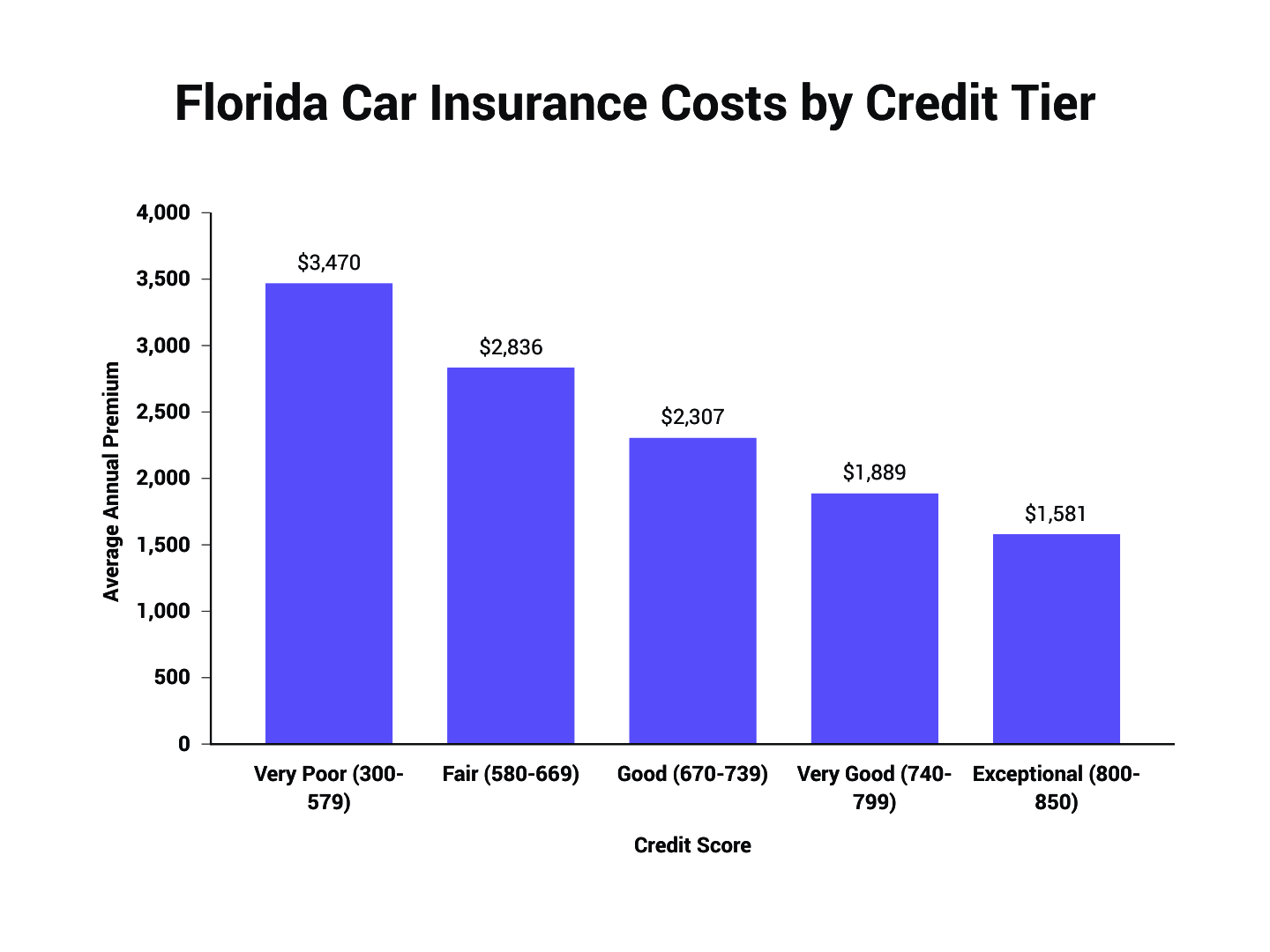

Insurers also consider your credit score in [Florida]. While some states prohibit this, in [Florida], a lower credit-based insurance score often correlates with higher premiums, as studies suggest a link between creditworthiness and the likelihood of filing a claim. Your marital status can also influence rates, with married individuals often receiving slightly lower premiums.

The type of vehicle you drive also has a substantial impact. High-performance cars, luxury vehicles, and models that are frequently stolen or costly to repair will typically incur higher insurance costs. Conversely, vehicles with excellent safety ratings, anti-theft devices, and lower repair costs often qualify for more favorable rates. Before purchasing a vehicle in [Florida], especially if you’re planning a longer stay or relocation, it’s wise to get insurance quotes for different models to understand their cost implications.

Location, Location, Location: How Florida Cities Influence Rates

Where you live within [Florida] can dramatically affect your car insurance rates. Urban areas, especially those with high population densities, heavy traffic congestion, higher rates of vehicle theft, and more frequent accidents, tend to have the most expensive premiums. For example, car insurance rates in cities like [Miami], [Fort Lauderdale], and [Orlando] are consistently among the highest in the state, and often in the nation. This is due to a confluence of factors: more vehicles on the road increase the probability of accidents, denser populations lead to more claims, and higher crime rates can translate to more comprehensive claims for theft or vandalism.

Conversely, residents in more suburban or rural areas, such as parts of [Sarasota], [Naples], or smaller towns in the panhandle, often enjoy lower rates. These areas typically have less traffic, fewer accidents, and lower crime rates. If you’re considering a move to [Florida] or planning an extended stay, researching insurance costs in potential residential areas should be a key part of your budget planning. Even within a large city, rates can vary by zip code, so it’s always worth getting specific quotes for your exact address. This geographical variance means that your chosen destination for a long-term [Florida] lifestyle, whether it’s beachfront living in [Palm Beach] or a quieter community near [Ocala National Forest], will directly influence one of your major monthly expenses.

Beyond the Basics: Optional Coverage for Peace of Mind

While [Florida] mandates PIP and PDL, these coverages offer limited protection. For true peace of mind, especially when navigating unfamiliar roads or protecting a significant investment like your vehicle, additional optional coverages are highly recommended.

- Collision Coverage: This pays for damage to your own vehicle resulting from a collision with another car or object, regardless of who is at fault. It’s essential if you want your car repaired or replaced after an accident.

- Comprehensive Coverage: This covers damage to your vehicle from non-collision incidents, such as theft, vandalism, fire, hail, floods (a significant concern in [Florida] due to hurricanes and heavy rains), falling objects, or hitting an animal. Given [Florida]’s climate and potential for severe weather, comprehensive coverage is often considered indispensable.

- Uninsured/Underinsured Motorist (UM/UIM) Coverage: Despite mandatory insurance laws, [Florida] has a significant number of uninsured drivers. UM/UIM protects you if you’re involved in an accident with a driver who doesn’t have insurance or whose insurance isn’t enough to cover your medical bills or vehicle damage. This coverage is crucial for protecting yourself and your family financially.

- Medical Payments (MedPay): Similar to PIP, MedPay can cover medical expenses for you and your passengers after an accident, regardless of fault. It can sometimes supplement PIP coverage or pay for expenses not covered by PIP.

- Rental Car Reimbursement: If your car is being repaired due to a covered claim, this coverage helps pay for a rental car. This is particularly useful for travelers or those relying on their vehicle for daily activities.

- Roadside Assistance: This covers services like towing, jump-starts, tire changes, and lockout services. While often available through other memberships, adding it to your policy can be convenient.

For anyone traveling extensively throughout [Florida] or planning to reside there, these optional coverages provide a robust safety net, protecting your finances and ensuring minimal disruption to your plans should an unforeseen incident occur.

Smart Strategies for Saving on Car Insurance in Florida

Given [Florida]’s relatively high insurance costs, finding ways to save money without compromising essential coverage is a priority for many drivers. Fortunately, there are several effective strategies that can significantly reduce your premiums, allowing you to allocate more of your budget towards enjoying [Florida]’s attractions, from the [Kennedy Space Center Visitor Complex] to the beaches of [Clearwater].

Discounts and Bundles: Maximizing Your Savings

Insurance companies offer a wide array of discounts designed to reward safe driving habits, customer loyalty, and various affiliations. Actively inquiring about and qualifying for these discounts can lead to substantial savings.

- Safe Driver Discount: Maintaining a clean driving record for a certain period (e.g., three or five years) can earn you a discount. Some insurers offer telematics programs that monitor your driving habits (speed, braking, mileage) via a device or app, providing discounts for safe driving.

- Multi-Policy Discount (Bundling): One of the most common and significant discounts is bundling your car insurance with other policies, such as homeowners, renters, or even boat insurance, with the same provider. If you’re considering a longer stay or relocation, this is an excellent way to consolidate and save.

- Good Student Discount: If you have a student driver on your policy who maintains a certain GPA, they may qualify for this discount.

- Anti-Theft Device Discount: Vehicles equipped with approved anti-theft systems (e.g., car alarms, tracking devices) often receive a discount due to reduced theft risk.

- Low Mileage Discount: If you don’t drive frequently, perhaps because you mostly use public transport in cities like [Jacksonville] or [St. Petersburg], or work from home, you might qualify for a low mileage discount.

- Defensive Driving Course Discount: Completing an approved defensive driving course can not only improve your driving skills but also potentially lower your premiums.

- Military Discount: Active duty military personnel, veterans, and their families may be eligible for special discounts with certain insurers.

- Senior Discount: Some companies offer discounts for older drivers who complete approved refresher courses.

Always ask your insurance agent about all available discounts. Even seemingly small discounts can add up, making a noticeable difference in your annual premium.

Comparing Quotes: The Key to Unlocking Better Rates

Perhaps the most powerful tool at your disposal for saving on car insurance is actively comparing quotes from multiple insurance providers. The insurance market in [Florida] is competitive, with numerous companies vying for your business, including national giants and regional specialists. Each insurer uses its own proprietary formulas to calculate risk and premiums, meaning that the same coverage for the same driver can vary significantly from one company to another.

Don’t settle for the first quote you receive. Utilize online comparison tools, or work with an independent insurance agent who can shop around on your behalf. It’s recommended to compare quotes at least once a year, or whenever there’s a significant life event such as moving to a new [Florida] city, buying a new car, or adding a new driver to your policy. When comparing, ensure you’re getting quotes for identical coverage amounts and deductibles to allow for a true apples-to-apples comparison. This diligent approach can uncover hundreds, if not thousands, of dollars in annual savings, freeing up funds to experience more of [Florida]’s vibrant culture, from the thrills of [Busch Gardens Tampa Bay] to the tranquil beauty of its countless natural springs.

Car Insurance and Your Florida Lifestyle: Budgeting for Your Adventure

Whether you’re a tourist embarking on a grand [Florida] road trip, a seasonal visitor enjoying the winter months, or a new resident establishing roots, car insurance will be a crucial component of your financial planning. Integrating these costs into your overall budget is vital for a stress-free and enjoyable [Florida] experience.

Planning Your Florida Trip: Integrating Insurance into Your Travel Budget

For short-term visitors renting a car, understanding rental car insurance options is key. Rental car companies typically offer various insurance products at the counter, such as Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW), Supplemental Liability Insurance (SLI), and Personal Accident Insurance (PAI). While convenient, these can be expensive.

Before you rent, check with your personal auto insurance provider; your existing policy might extend coverage to a rental car, especially for liability. Many credit cards also offer secondary collision/loss damage waiver benefits when you use their card to pay for the rental. Carefully review your credit card’s benefits guide and confirm with them directly, as coverage levels and exclusions vary widely. For international visitors, purchasing a short-term policy or ensuring your home country’s insurance provides adequate coverage in the [United States] is essential. Neglecting rental car insurance can lead to significant financial exposure in the event of an accident, potentially derailing your entire [Florida] vacation. Planning this aspect ensures that your focus remains on exploring the beautiful [Florida] beaches and attractions, rather than worrying about unforeseen expenses.

Considering a Florida Move: Long-Term Insurance Implications

For those considering a permanent move to [Florida], car insurance is a significant financial factor that must be budgeted for. Once you establish residency in [Florida], you’ll be required to register your vehicle in the state and obtain a [Florida] driver’s license. At this point, you’ll need to secure a car insurance policy from a company licensed to operate in [Florida].

This transition can sometimes lead to a noticeable change in your premiums, especially if you’re moving from a state with lower average rates. It’s crucial to obtain quotes from several [Florida] insurers before your move to accurately forecast this expense. Factor in the specific [Florida] city or town you’re considering, as location heavily influences rates. Understanding these long-term insurance implications is as important as researching housing costs or employment opportunities when planning your new [Florida] lifestyle. It ensures you have a realistic picture of your monthly expenses and can budget effectively to fully embrace all that the Sunshine State has to offer, from its diverse cultural scene to its endless outdoor adventures.

In conclusion, while the question “how much is car insurance in [Florida]?” might initially seem daunting due to higher-than-average costs, a thorough understanding of the state’s requirements, the factors influencing premiums, and proactive shopping strategies can make it a manageable part of your [Florida] budget. Whether you’re visiting for a week or planning a lifetime in the Sunshine State, being an informed consumer of car insurance will ensure your journeys are safe, secure, and financially sound, allowing you to truly immerse yourself in the vibrant tapestry of [Florida] life.