Florida, often celebrated as the Sunshine State, beckons millions of visitors annually with its pristine beaches, vibrant cities, and world-class attractions. From the magical theme parks of Orlando to the art deco charm of Miami Beach and the tranquil Gulf Coast havens of Naples, the state offers an unparalleled lifestyle and diverse travel experiences. However, beneath this sun-drenched facade lies a crucial consideration for anyone contemplating extended stays, property ownership, or even just frequent visits: the inherent risk of flooding and the necessity of flood insurance.

Understanding the cost and complexities of flood insurance in Florida is not just for homeowners; it’s a vital piece of information for real estate investors eyeing a new hotel, families considering a long-term rental, or even individuals planning a significant move. The financial implications of a flood event can be devastating, far exceeding the typical coverage of standard homeowners’ policies. This article delves into the nuances of flood insurance costs in Florida, exploring the factors that drive premiums and offering insights relevant to property owners, tourism operators, and anyone whose lifestyle or travel plans are tied to this beautiful, yet vulnerable, peninsula.

Understanding Florida’s Unique Flood Risk Landscape

Florida’s geography is both its greatest asset and its most significant challenge when it comes to water. Bordered by the Atlantic Ocean to the east and the Gulf of Mexico to the west, with thousands of miles of coastline, countless lakes, and extensive river systems, the state is intrinsically linked to water. This aquatic abundance, while stunning for tourism and recreation, also positions Florida at a perpetually high risk of flooding.

Why Florida is a Flood Hotspot

The reasons for Florida’s susceptibility to flooding are multifaceted and deeply rooted in its natural environment and climatic patterns.

Firstly, geographic factors play a pivotal role. Much of Florida is incredibly low-lying, with an average elevation that makes it particularly vulnerable to rising sea levels and storm surges. Coastal communities, from the lively streets of Key West to the urban sprawl of Fort Lauderdale, face constant threats from high tides and the encroaching ocean. Even inland areas, such as those around Orlando, can experience significant flooding due to heavy rainfall overwhelming drainage systems and rivers overflowing their banks.

Secondly, climatic factors, particularly during hurricane season (June 1st to November 30th), dramatically increase flood risks. Florida is the most hurricane-prone state in the United States. These powerful tropical storms bring not only destructive winds but also torrential rainfall and catastrophic storm surges that can inundate vast areas. Even less intense tropical depressions and severe thunderstorms can lead to localized flooding, disrupting daily life, travel plans, and business operations.

The pervasive flood risk has a profound impact on Florida’s tourism infrastructure and real estate market. A major hurricane or flood event can shut down airports, close roads like the iconic Florida Keys Overseas Highway, and force the evacuation or closure of hotels, resorts, and popular attractions. For instance, a flood affecting a coastal landmark or a luxurious resort could lead to significant financial losses and reputational damage. Property values in high-risk areas are directly influenced by the availability and cost of flood insurance, making it a critical consideration for anyone looking to invest in a vacation rental, a second home, or even a commercial accommodation venture. Understanding this inherent risk is the first step toward safeguarding investments and ensuring peace of mind in the Sunshine State.

Decoding Flood Insurance Costs: What to Expect

When considering flood insurance in Florida, prospective buyers and current property owners quickly discover that there isn’t a single, flat rate. Premiums are highly individualized, reflecting a complex interplay of factors designed to assess the specific risk profile of a property. This individualized pricing model, especially under the latest FEMA rating system, aims for greater equity, but it also necessitates a thorough understanding of what influences your potential costs.

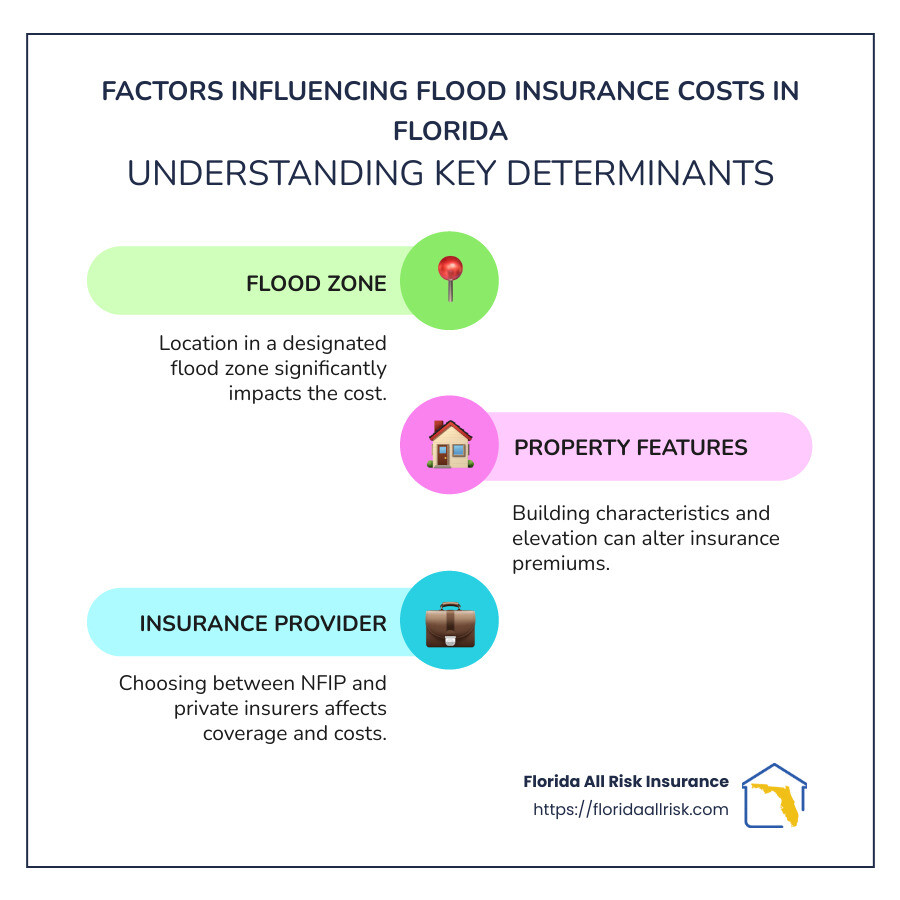

Key Factors Influencing Premiums

Several critical elements determine how much you will pay for flood insurance, whether through the National Flood Insurance Program (NFIP) or the burgeoning private market.

- Flood Zone: This is perhaps the most significant factor. FEMA designates flood zones based on the likelihood of a flood occurring. Properties in high-risk zones, such as Zone A (areas with a 1% annual chance of flooding) or Zone V (coastal areas with velocity hazards), will face higher premiums. Conversely, properties in moderate-to-low-risk areas, like Zone X, generally have lower rates, though flood insurance is still highly recommended even there.

- Building Elevation: For properties in high-risk zones, the elevation of the lowest floor relative to the Base Flood Elevation (BFE) is crucial. A home built above the BFE will typically have lower premiums than one built below it. This is where an Elevation Certificate becomes indispensable, providing detailed information about your property’s elevation.

- Building Characteristics: The age of the building, its construction materials, foundation type (e.g., slab, crawl space, pilings), and the number of floors all play a role. Older homes, or those built with less flood-resistant materials, may incur higher costs.

- Coverage Amount and Deductible: Like other insurance policies, the amount of coverage you purchase for your structure and its contents directly impacts the premium. Choosing a higher deductible (the amount you pay out-of-pocket before insurance kicks in) can lower your annual premium, but means greater upfront costs if a flood occurs.

- Property Use: Whether the property is a primary residence, a vacation home, or a commercial establishment (like a hotel or resort) can influence the rate, especially in the private market.

- Location within Florida: While the entire state is susceptible, specific cities and counties face differing risk levels. Premiums can vary significantly between coastal hubs like Miami or Tampa and more inland areas or less developed coastlines.

Average Costs and Policy Options

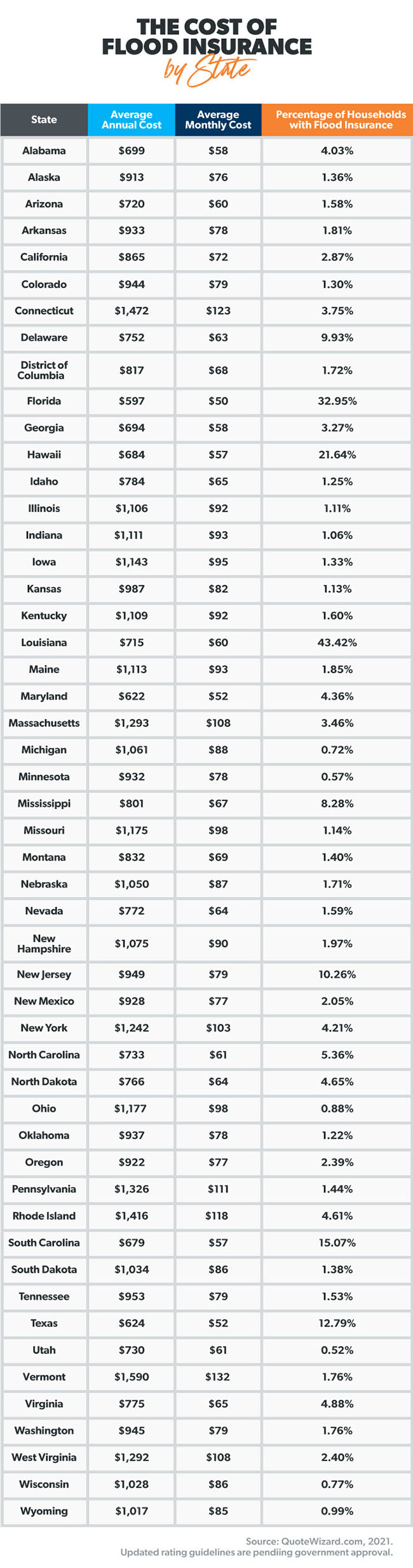

Prior to FEMA’s implementation of Risk Rating 2.0 in 2021-2022, average flood insurance premiums in Florida were often cited in the range of $600 to $1,000 annually, though these averages could be misleading due to deep subsidies for older properties. Under Risk Rating 2.0, the pricing model shifted to be more equitable and individualized, reflecting each property’s specific flood risk rather than broad flood zones. This means some properties, particularly those with previously subsidized rates in high-risk areas, have seen significant increases, while others in lower-risk areas might see decreases or modest changes.

Today, it’s more accurate to say that flood insurance costs in Florida can range from a few hundred dollars annually for properties in low-risk Zone X up to several thousand dollars per year for high-value properties in severe flood zones. For instance, a homeowner in a high-risk coastal area like Sarasota could easily pay $2,000-$5,000 or more annually, especially for a large or older property, while a smaller home in a moderate-risk area of Jacksonville might pay closer to $700-$1,500.

There are primarily two avenues for obtaining flood insurance:

- The National Flood Insurance Program (NFIP): Administered by FEMA, the NFIP is the primary source of flood insurance for many United States residents. It offers standardized policies and is often mandatory for properties with federally backed mortgages located in high-risk flood zones.

- Private Flood Insurance: In recent years, a growing private market for flood insurance has emerged, particularly in Florida. Private policies can sometimes offer broader coverage, higher limits than the NFIP ($250,000 for building, $100,000 for contents), and potentially more competitive pricing for certain risk profiles. It’s highly recommended to compare quotes from both the NFIP and private insurers.

It’s crucial to remember that a standard homeowners’ insurance policy does not cover flood damage. This is a common misconception that can lead to devastating financial losses. If you have a federally backed mortgage and your property is in a high-risk flood zone, flood insurance is mandatory. However, even if it’s not mandated, the peace of mind and financial protection it offers are invaluable in a state as prone to flooding as Florida.

The Intersection of Flood Insurance, Travel, and Accommodation in Florida

The discussion around flood insurance in Florida extends far beyond individual homeowners. It intricately weaves into the fabric of the state’s massive tourism industry, influencing everything from the viability of hotel investments to the experiences of transient visitors. Understanding this intersection is critical for anyone engaging with Florida’s vibrant accommodation and travel sectors.

Protecting Your Florida Investment and Travel Plans

For many, Florida represents an ideal location for investment, whether in a sprawling resort, a boutique hotel, a charming vacation rental, or a cherished second home. For these property owners and investors, flood insurance is not merely a regulatory requirement; it’s a non-negotiable safeguard.

- For Property Owners/Investors (Hotels, Vacation Rentals, Second Homes): Owning accommodation in Florida means embracing the unique opportunities and inherent risks of the region. A multi-million dollar asset like the iconic Breakers Palm Beach, a collection of luxury villas in Miami, or even a modest Airbnb in historic St. Augustine can face significant financial exposure from flood damage. Comprehensive flood insurance protects these critical investments against structural damage, damage to contents, and potentially business interruption costs, ensuring the longevity and profitability of the venture. Without it, a single flood event could wipe out years of equity and investment, severely impacting the broader lifestyle associated with such ownership.

- For Tourists and Long-term Stays: While individual tourists are not typically purchasing flood insurance for their short stays, the existence and robustness of flood insurance policies for the properties they occupy directly impact their travel experience and safety. Hotels and resorts, especially those in prime coastal locations, must have adequate coverage to quickly recover from flood events, minimizing disruptions to guest services and ensuring a swift return to operation. Travelers booking accommodation in Florida, particularly during hurricane season, should always consider travel insurance that includes coverage for natural disasters and look for hotels with transparent cancellation policies. Understanding the flood risk of their chosen destination can help in making informed decisions about where to stay and what precautions to take, ensuring a smooth and worry-free vacation.

- Impact on Tourism Infrastructure: Beyond individual properties, flood events can paralyze essential tourism infrastructure. Roads, bridges, airports, and public transportation networks can become impassable, directly affecting travelers’ ability to reach their destinations or move between attractions. Significant landmarks or natural areas popular with tourists might close for extended periods for repairs or safety assessments. This disruption has a ripple effect, impacting local businesses, restaurants, and activity providers that rely on tourist footfall. Robust flood preparedness and insurance for public infrastructure and private enterprises are therefore crucial for maintaining Florida’s reputation as a premier travel destination and supporting the lifestyle of its residents and visitors alike.

Strategies for Managing Flood Insurance Costs

Given the essential nature of flood insurance in Florida, both for property protection and peace of mind, exploring ways to manage or potentially reduce its cost is a wise endeavor for residents and business owners alike. While you cannot change your property’s inherent flood risk, several proactive steps can positively influence your premiums.

Practical Tips for Residents and Business Owners

Implementing these strategies can not only lead to potential savings but also contribute to a more resilient property and community.

- Review and Understand Flood Maps: Regularly check the FEMA flood maps for your area. Understanding your current flood zone, and any potential changes, is the first step in assessing your risk and insurance needs. These maps are dynamic and can be updated, potentially changing your premium.

- Obtain or Update an Elevation Certificate (EC): An accurate Elevation Certificate is invaluable, especially for properties in high-risk zones. It details the elevation of your home or building relative to the Base Flood Elevation (BFE). If your home is built higher than officially recorded, an updated EC could significantly lower your premium under NFIP’s Risk Rating 2.0 or even with private insurers.

- Implement Flood Mitigation Measures: Proactively making your property more flood-resistant can lead to lower premiums and, more importantly, reduced damage in the event of a flood. This includes:

- Elevating utilities: Raising electrical panels, water heaters, and HVAC systems above the BFE.

- Installing flood vents: For properties with crawl spaces or enclosed foundations, flood vents allow water to flow through, reducing hydrostatic pressure on walls.

- Using flood-resistant materials: For renovations or new construction, choosing materials resistant to flood damage can be a long-term cost saver.

- Elevating the structure: For new construction or substantial renovations, elevating the entire structure on pilings or a raised foundation is the most effective mitigation strategy.

- Compare Policies from NFIP and Private Insurers: Don’t settle for the first quote. The private flood insurance market in Florida is competitive and expanding. Private policies may offer broader coverage, higher limits, or more favorable pricing for certain properties compared to the NFIP. Always get multiple quotes to ensure you’re getting the best value.

- Choose Deductibles Wisely: A higher deductible on your flood insurance policy will generally result in a lower annual premium. However, be sure you have enough in your emergency fund to cover that deductible if a flood occurs.

- Inquire About the Community Rating System (CRS): Some communities in Florida participate in FEMA’s Community Rating System (CRS). This voluntary program encourages communities to implement floodplain management practices that exceed the minimum NFIP requirements. In return, NFIP policyholders in these communities receive discounts on their flood insurance premiums. Check if your city or county is a CRS participant.

By taking these steps, Florida residents, business owners, and those managing accommodation properties can gain a clearer understanding of their flood risk, potentially reduce their insurance costs, and ultimately protect their assets against the unpredictable forces of nature in the Sunshine State.

In conclusion, while the allure of Florida’s travel, hotels, tourism, accommodation, landmarks, and lifestyle is undeniable, the state’s inherent vulnerability to flooding necessitates a proactive approach to protection. Understanding “how much is flood insurance in Florida” is more than just a question of cost; it’s a vital component of responsible property ownership, strategic business planning in the hospitality sector, and ensuring peace of mind for anyone who calls Florida home or a cherished destination. By staying informed about flood risks, exploring available policy options, and implementing mitigation strategies, individuals and businesses can safeguard their investments and continue to enjoy all that the Sunshine State has to offer, come rain or shine.