The allure of California is undeniable. From its sun-drenched beaches and iconic landmarks to its vibrant cities and breathtaking natural beauty, the Golden State has long captivated the imaginations of travelers, dreamers, and those seeking a permanent slice of paradise. Whether you’re considering a luxurious long-term stay, investing in a vacation rental, or even dreaming of owning a piece of this sought-after landscape, understanding the financial nuances of property ownership is paramount. Among the most significant considerations for any property owner or prospective investor in California is the property tax. This often-complex system can significantly impact the overall cost of living, the profitability of a rental property, or the long-term viability of a second home. For those venturing into the world of California real estate, be it a cozy apartment in San Francisco, a sprawling estate in Beverly Hills, or a charming bungalow in San Diego, deciphering the property tax structure is the first crucial step. This comprehensive guide aims to demystify property taxes in California, providing clarity for anyone considering making this beautiful state their home, a temporary retreat, or a strategic investment. We’ll explore the foundational principles, additional charges, how these taxes influence lifestyle and travel choices, and potential avenues for relief or planning.

Understanding the Golden State’s Property Tax System

At the heart of California’s property tax system lies a historical and often misunderstood piece of legislation: Proposition 13. Enacted in 1978, this constitutional amendment fundamentally reshaped how properties are assessed and taxed, creating a system that is distinct from many other states. Its primary goal was to provide property tax relief and predictability for homeowners, but it has also led to unique dynamics in the state’s real estate market.

Proposition 13: The Foundation of California’s Property Tax

Proposition 13 establishes the baseline for property tax calculations. It dictates that the maximum ad valorem tax on real property cannot exceed one percent (1%) of its “full cash value.” This full cash value is generally defined as the county assessor’s valuation of the property as shown on the 1975-76 tax bill, or the appraised value when the property is purchased, newly constructed, or a change in ownership occurs after 1975.

Crucially, Proposition 13 also limits the annual increase in a property’s assessed value. Even with rising market values, the assessed value for tax purposes can only increase by a maximum of two percent (2%) per year, or the percentage change in the California Consumer Price Index, whichever is less. This means that if you’ve owned your property for many years, its assessed value for tax purposes is likely significantly lower than its current market value, offering substantial tax savings. This aspect of Proposition 13 is often cited as a major benefit for long-term residents and can be a significant draw for those planning an extended stay or retirement in the state. However, it also means that new buyers entering the market will face property taxes based on the current purchase price, which can be considerably higher.

How Property Value is Assessed

The assessment process begins with the county assessor’s office, which is responsible for determining the “full cash value” of properties within its jurisdiction. For new purchases, this is straightforward: the sales price typically becomes the new assessed value. For properties that haven’t changed ownership or undergone significant construction, the assessor annually adjusts the base year value by the Proposition 13 inflation factor, capped at 2%.

Understanding this assessment methodology is vital. If you’re looking at properties in desirable areas like Malibu or Napa Valley, the purchase price will directly translate into a high base assessed value, leading to a substantial initial property tax bill. Conversely, an older property in a less rapidly appreciating market like parts of Sacramento might have a much lower effective tax rate relative to its current market value, making it potentially more attractive for those on a tighter budget. For potential investors eyeing the robust rental markets in cities like Los Angeles or Santa Monica, this means factoring in a property tax bill that reflects the current market value, not just the advertised 1% base rate.

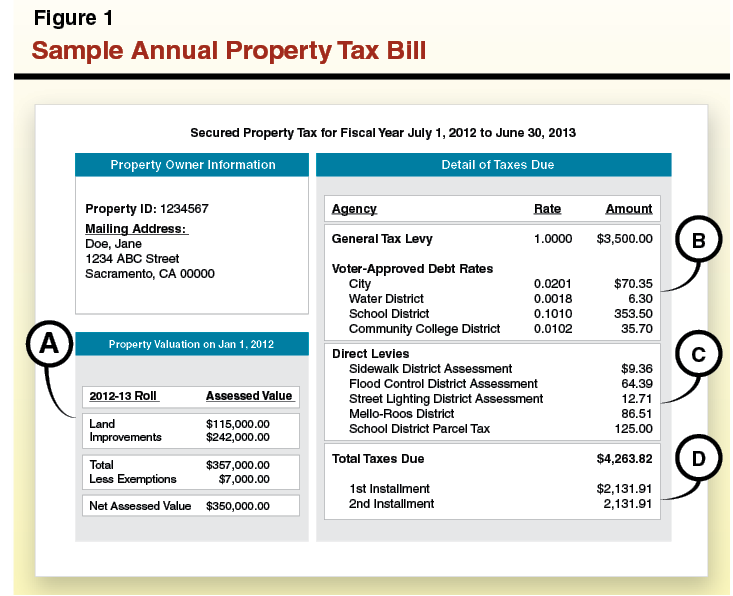

Beyond the Base Rate: Special Assessments and Additional Charges

While Proposition 13 sets the foundational 1% rate, it’s crucial to understand that your total property tax bill will almost certainly be higher due to a variety of additional charges. These “add-on” assessments are not limited by Proposition 13’s 1% cap or 2% annual increase limit, making them a significant factor in the overall tax burden.

Mello-Roos and Other Local Bonds

One of the most common additions to a California property tax bill is the Mello-Roos Community Facilities Act tax. Mello-Roos districts are special tax districts created by local governments (cities, counties, or school districts) to finance new infrastructure projects or services for a specific area. These can include schools, parks, roads, libraries, police and fire protection, and more. Properties within a Mello-Roos district will pay an additional tax on top of their regular property tax bill.

These assessments are particularly common in newer developments and master-planned communities across the state, such as those found in parts of Orange County or emerging areas in the Inland Empire. For travelers considering a long-term rental or the purchase of a newer vacation home, especially near family-friendly attractions like Disneyland or resort communities, it’s imperative to check for Mello-Roos taxes. These can add anywhere from a few hundred to several thousand dollars annually to a property tax bill, pushing the effective rate well above the 1% base. Other local bonds for schools, water districts, or transportation projects can similarly increase the overall tax burden.

Supplemental Taxes: What to Expect

When a property changes ownership or new construction is completed, a supplemental property tax bill is often issued. This occurs because the county assessor must revalue the property to its new “full cash value” (usually the sale price or new construction value) as of the date of the change in ownership or completion of construction.

Since property tax bills are typically issued annually based on the previous fiscal year’s assessment, there’s often a gap between the reassessment event and the issuance of the next regular tax bill. The supplemental tax bill covers this gap, calculating the additional tax owed from the date of change until the end of the current tax year. For new homeowners or investors, it’s crucial to budget for this supplemental bill, which can arrive unexpectedly several months after closing escrow. This is particularly relevant for those acquiring vacation properties or short-term rental units, as it represents an immediate, albeit temporary, additional cost not always factored into initial budgeting.

The Impact of Property Transfers and New Construction

Any “change in ownership” or “new construction” triggers a reassessment of the property to its current market value, effectively resetting the Proposition 13 base year value.

- Change in Ownership: Most sales or transfers of property constitute a change in ownership. Exceptions exist for transfers between parents and children or grandparents and grandchildren (under certain conditions), and transfers between spouses. These exceptions can be particularly valuable for families planning multi-generational living or the inheritance of a vacation home in popular destinations like Lake Tahoe or Palm Springs, allowing the lower assessed value to be retained.

- New Construction: Significant additions, remodels, or completely new structures are considered “new construction.” Only the newly constructed portion or the value added by the remodel is reassessed to current market value. This is important for those looking to customize a property for their specific lifestyle or to enhance a rental unit for higher tourism appeal. The added value of a new guest house, a swimming pool, or an extensive renovation will increase the assessed value and thus the property taxes for that specific improvement.

Property Tax and Your California Lifestyle: From Travel to Accommodation

The intricacies of California property taxes extend far beyond mere financial calculations; they significantly influence lifestyle choices, travel decisions, and investment strategies. For a website focused on travel, hotels, tourism, and accommodation, understanding these impacts is crucial for guiding potential visitors, long-term residents, and investors.

Choosing Your California Destination: Tax Implications for Homeowners and Investors

Where you choose to settle or invest in California can have a dramatic effect on your property tax burden. High-demand areas like Silicon Valley, Orange County, and coastal Los Angeles (e.g., Malibu, Laguna Beach) command astronomical property values, meaning even the 1% base rate translates to a substantial annual tax. When coupled with potential Mello-Roos taxes for newer communities, the total effective rate can be closer to 1.25% to 1.5% or even higher in some areas, especially when accounting for parcel taxes for local services.

For travelers considering a permanent move or the purchase of a second home, this means evaluating locations not just for their amenities and lifestyle, but also for their tax profiles. A property near Universal Studios Hollywood might seem appealing for entertainment access, but the premium price will lead to a higher tax bill. Alternatively, less expensive regions like parts of the Central Valley or mountain communities near Yosemite National Park might offer lower entry prices and thus lower property tax bills, making them more accessible for budget-conscious buyers or those seeking a quieter lifestyle. For investors, the long-term appreciation potential must be weighed against the annual carrying costs, with property taxes being a major component.

Long-Term Stays and Rental Properties: Navigating the Tax Landscape

For those considering long-term accommodation in California, whether as renters or property owners, property taxes play a hidden but significant role. Property owners often pass on a portion of their property tax burden to renters in the form of higher rental prices. Thus, understanding the tax environment can help renters gauge the underlying cost pressures in different markets.

For investors in the short-term or long-term rental market, property taxes are a fixed, ongoing expense that directly impacts profitability. A savvy investor looking to purchase a multi-unit property in a bustling city like San Francisco or a charming vacation rental in Palm Springs must meticulously calculate these costs. High property taxes can erode rental income, especially in areas where rent control measures limit income growth. Conversely, properties purchased decades ago with low base year values can offer exceptional cash flow due to their significantly lower tax liabilities. This disparity often creates a barrier to entry for new investors, who face a much higher property tax burden than long-term owners.

Luxury Resorts and Vacation Homes: A Closer Look at High-Value Properties

The luxury travel sector in California thrives on opulent accommodations, from private villas in Laguna Beach to exclusive suites at a Ritz-Carlton or Four Seasons resort. Many affluent travelers consider purchasing vacation homes or fractional ownership in these high-end destinations. For these high-value properties, property taxes become an even more substantial annual expense.

Consider a multi-million dollar vacation home in Lake Tahoe or Santa Barbara. Even at a nominal 1.1% or 1.2% effective tax rate, the annual property tax bill could easily be tens of thousands of dollars. This cost is a critical component of the overall “lifestyle tax” associated with luxury property ownership in California. It influences decisions such as how often the property is used, whether it’s placed in a rental pool, and the long-term financial viability for the owner. Understanding these significant recurring costs is essential for anyone considering investing in the state’s vibrant luxury real estate market.

Exemptions, Appeals, and Planning for Your California Dream

Navigating the California property tax system isn’t just about understanding the bills; it’s also about leveraging available exemptions, knowing your rights to appeal assessments, and strategically planning for long-term ownership.

Key Exemptions That Can Save You Money

Several exemptions can help reduce your property tax bill, with the most common being the Homeowners’ Exemption.

- Homeowners’ Exemption: If you own and occupy your home as your principal place of residence, you can apply for a Homeowners’ Exemption, which reduces the assessed value of your property by $7,000. While this may seem modest in the context of California’s high property values, it translates to an annual tax savings of approximately $70 to $80. Every little bit counts, especially for those on fixed incomes or those making their primary residence in more affordable cities like Ventura County.

- Disabled Veterans’ Exemption: Eligible disabled veterans or their unmarried surviving spouses can receive a much more substantial exemption, which can be basic or low-income, significantly reducing their tax burden. This exemption acknowledges the service of veterans and helps make homeownership more accessible for those who have sacrificed for their country.

- Other Exemptions: Various other exemptions exist for properties used for religious, charitable, hospital, or educational purposes. While less relevant for individual homeowners, these play a crucial role in the overall tax landscape and public services.

It’s important to apply for these exemptions, as they are not automatically granted. New homeowners should contact their county assessor’s office shortly after purchase to ensure they receive any eligible reductions.

Appealing Your Property Assessment

Property owners in California have the right to appeal their property’s assessed value if they believe it is incorrect. This usually occurs when a property’s market value has significantly declined, falling below its current assessed value. This situation, though less common in California’s generally appreciating market, can happen during economic downturns or in specific localized conditions.

The appeal process typically involves filing an application with the county Assessment Appeals Board. Owners must provide evidence that their property’s market value is lower than the assessor’s value as of the lien date (January 1st). This evidence often includes comparable sales of similar properties in the area. For investors or vacation home owners who track market fluctuations closely, being proactive about appeals can lead to considerable tax savings. It’s a critical tool for managing costs, particularly in volatile real estate markets.

Financial Planning for California Property Ownership

Owning property in California is a significant financial undertaking, and careful planning is essential. Beyond the purchase price and mortgage, property taxes are a substantial, ongoing cost that must be factored into any budget.

For prospective buyers, especially those new to the state, it’s vital to research the specific tax rates and potential Mello-Roos assessments for any neighborhood they are considering. Online resources from county assessor’s offices or real estate listing sites often provide estimated tax information. For investors, a clear understanding of property taxes is paramount for calculating potential returns on investment, especially for properties intended for short-term tourism or long-term rental income. Furthermore, estate planning can also involve considerations related to Proposition 13’s reassessment rules, as transferring property to heirs can sometimes trigger a reassessment unless specific exclusions apply.

In conclusion, while the dream of California property ownership is enticing, a thorough understanding of its unique property tax landscape is crucial. From the foundational principles of Proposition 13 and the impact of special assessments to the strategic considerations for lifestyle, travel, and investment, deciphering “how much is property tax in California” is a complex but navigable journey. With careful research and informed planning, the Golden State’s captivating charm can become a financially viable reality.