California, a state renowned for its breathtaking landscapes, vibrant cities, and diverse lifestyle options, attracts millions of residents and visitors annually. Whether you’re settling into a beachfront apartment in Santa Monica, a trendy loft in downtown Los Angeles, a historic Victorian in San Francisco, or a spacious family home in Sacramento, securing your personal space and belongings is paramount. While many focus on finding the perfect accommodation – be it stylish apartments, luxurious villas, or comfortable long-term suites – the often-overlooked necessity is renters insurance. It’s a vital safety net, protecting your possessions and providing liability coverage against unforeseen events.

Given the Golden State’s dynamic environment, from bustling urban centers to serene natural destinations, the question inevitably arises: “How much is renters insurance in California?” The answer, like much else in this vast state, isn’t a single figure but a range influenced by numerous factors. This comprehensive guide will explore the average costs, the elements that shape your premium, and practical tips for finding affordable coverage, ensuring your peace of mind whether you’re embarking on business stays, family trips, or simply enjoying a long-term residence amidst California’s myriad attractions.

Understanding the Landscape: Why Renters Insurance Matters in California

Living in California offers an unparalleled quality of life, but it also comes with unique considerations. From natural phenomena to the diverse socio-economic landscapes of its cities, protecting your personal sanctuary with renters insurance is a non-negotiable aspect of responsible living.

The Golden State’s Unique Appeal and Risks

California’s allure is undeniable. Tourists flock to its landmarks and experiences, while residents enjoy a vibrant local culture, world-class food, and endless activities. However, this beauty comes with its own set of risks. The state is susceptible to earthquakes, and while standard renters insurance doesn’t cover earthquake damage, the broader risk profile of the region can subtly influence insurance markets. Additionally, urban areas like Los Angeles, San Francisco, and San Diego can have higher rates of theft or vandalism, impacting insurance premiums. Accidental water damage, fire, and other perils are also common concerns regardless of location.

For those embracing the California dream, which often involves frequent relocations for work or leisure, renters insurance offers a crucial layer of security. Whether you’re a digital nomad living in a new apartment every few months or a student residing in a temporary rental for your studies, your belongings are valuable, and their protection should extend beyond the walls of your rented space. This peace of mind allows you to fully engage with the tourism and travel opportunities the state offers, knowing your home base is secure.

Beyond Landlords’ Policies: Protecting Your Personal Sanctuary

A common misconception among renters is that their landlord’s insurance policy will cover their personal belongings. This is false. A landlord’s policy typically covers the building structure and their liability, but it offers no protection for your furniture, electronics, clothing, or other personal items. Without renters insurance, if a fire, theft, or other covered peril occurs, you would be solely responsible for replacing everything you own.

Renters insurance typically includes three main components:

- Personal Property Coverage: This protects your belongings from specified perils, whether they are in your apartment or with you while traveling. This means if your laptop is stolen from your hotel room while on a trip to Yosemite National Park, it might be covered (subject to policy terms and deductibles).

- Liability Coverage: This protects you if someone is injured in your rental unit or if you accidentally cause damage to someone else’s property. For example, if a guest slips and falls in your apartment, or if your bathtub overflows and causes damage to the unit below, your liability coverage would help cover legal fees and medical expenses. This is especially important in a litigious state like California.

- Additional Living Expenses (ALE): If your rental unit becomes uninhabitable due to a covered loss (e.g., a fire), ALE coverage will help pay for temporary housing, hotel stays, meals, and other increased living costs while your apartment is being repaired or you find a new one. For individuals accustomed to luxury travel or comfortable accommodation, this ensures minimal disruption to their lifestyle.

Deconstructing the Cost: Key Factors Influencing Premiums

The cost of renters insurance in California is not uniform. Several variables come into play, influencing how much you’ll pay annually. Understanding these factors is key to navigating the comparison process and securing a policy that fits both your needs and your budget travel considerations.

Location, Location, Location: Urban vs. Suburban vs. Rural

Just as location dictates property values, it significantly impacts renters insurance premiums.

- Urban Centers: Cities like Los Angeles, San Francisco, and Oakland often have higher premiums due to increased population density, higher rates of theft, and greater exposure to certain risks. The cost of replacing belongings can also be higher in these areas.

- Suburban and Rural Areas: Communities outside major metropolitan hubs, such as Fresno, Bakersfield, or quieter towns in the Central Valley, might see lower rates due to lower crime statistics and potentially reduced overall risk.

- Natural Disaster Zones: While standard renters insurance doesn’t cover earthquakes or floods, living in areas prone to these events (e.g., coastal zones for floods, fault lines for earthquakes) can still indirectly influence premiums due to the overall risk perception and market conditions in that region.

This geographical variability highlights the importance of getting quotes specific to your exact address. For those who frequently move or engage in long-term stays across different California regions, understanding these local nuances is crucial for intelligent booking and insurance decisions.

Coverage Levels: What You Choose to Protect

The amount and type of coverage you select are primary drivers of your premium.

- Personal Property Coverage Amount: The higher the value of your possessions you want to protect, the higher your premium will be. It’s essential to conduct a home inventory to accurately estimate the value of your belongings.

- Actual Cash Value (ACV) vs. Replacement Cost Value (RCV): ACV policies pay out the depreciated value of your items, meaning you’ll get less than what it costs to buy new replacements. RCV policies, though slightly more expensive, pay out the cost to replace items with new ones of similar quality, offering superior protection. For those with a taste for fine architecture or valuable collections, RCV is often preferred.

- Liability Limits: Standard liability coverage is often $100,000, but you can increase it to $300,000 or even $500,000 for added protection, especially if you have significant assets to protect.

- Deductible: This is the amount you pay out-of-pocket before your insurance kicks in. Choosing a higher deductible (e.g., $1,000 instead of $500) will lower your premium, but you’ll pay more upfront if you file a claim.

- Riders/Endorsements: If you own particularly valuable items like fine jewelry, art, or high-end electronics that exceed standard coverage limits, you might need to add a “rider” or “endorsement” to your policy. This will increase your premium but ensures these specific items are fully protected. This is particularly relevant for those who enjoy luxury travel and carry valuable items.

Your Personal Profile and Building Characteristics

Individual factors and the specifics of your rental unit also play a role in premium calculation.

- Claims History: If you’ve filed multiple insurance claims in the past, insurers may view you as a higher risk, leading to higher premiums.

- Credit Score: In California, while credit-based insurance scores are regulated, they can still influence your premium to some degree. A good credit history often signals financial responsibility, potentially resulting in lower rates.

- Building Safety Features: Living in a building with robust security features can lead to discounts. This includes fire alarms, sprinkler systems, security systems, deadbolt locks, gated communities (common in many resorts or upscale apartment complexes), and on-site security personnel. Many modern apartments and villas feature these amenities as standard.

- Age and Construction of the Building: Older buildings might have higher premiums due to potential infrastructure issues, while newer constructions often benefit from updated safety codes and materials.

Average Costs and How to Save on Renters Insurance in California

Now, let’s get to the numbers. While rates vary significantly, understanding the typical range and how to reduce your costs is crucial for making an informed decision about your accommodation protection.

The Numbers: What to Expect

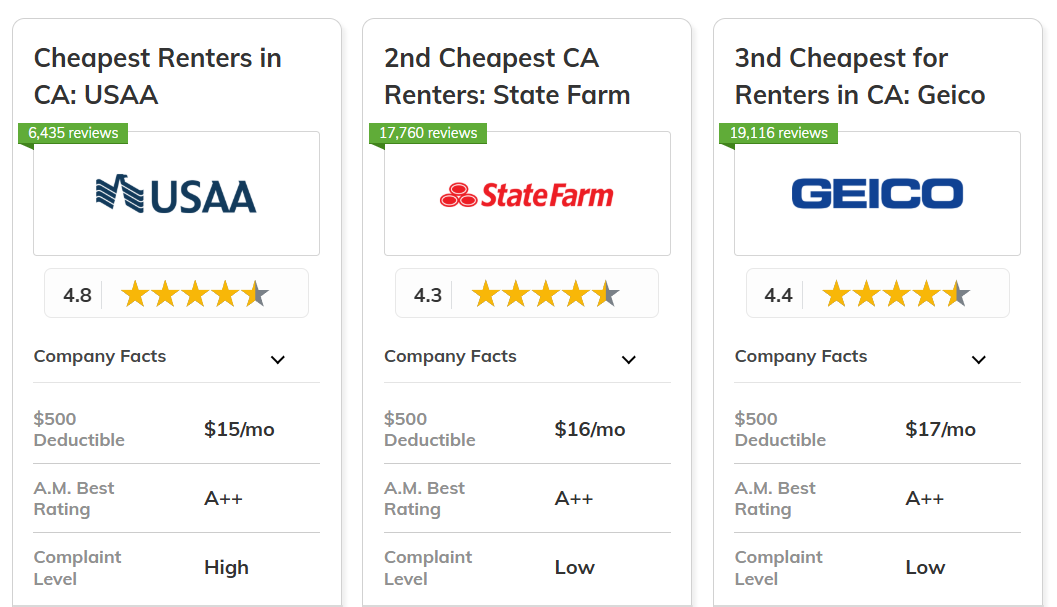

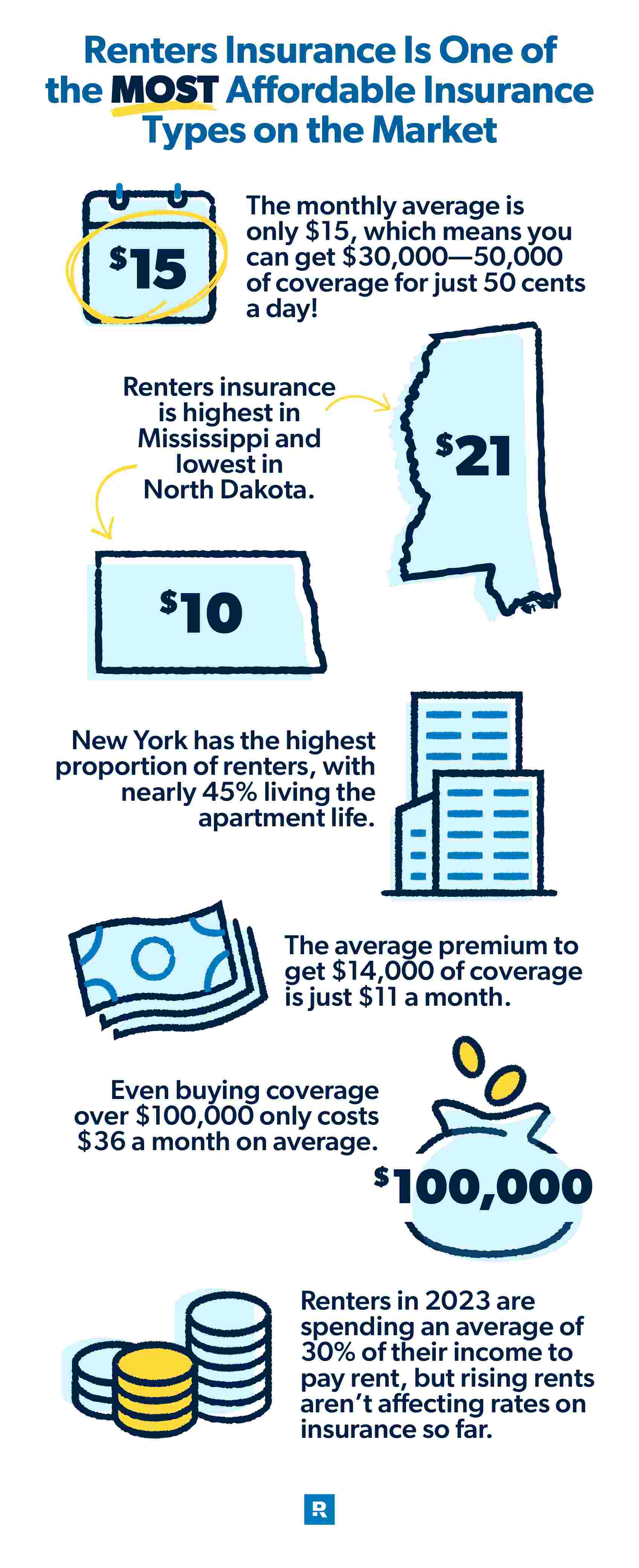

On average, renters insurance in California is quite affordable, especially when considering the protection it provides. Most residents can expect to pay between $15 to $25 per month, or roughly $180 to $300 annually.

However, this is a broad average. For a basic policy covering around $20,000 in personal property and $100,000 in liability with a $500 deductible:

- In a high-cost urban area like San Francisco or Los Angeles, you might pay closer to $20-$30 per month.

- In a more moderately priced city like Sacramento or Riverside, the cost could be in the $15-$20 range.

- In smaller towns or less densely populated areas like Fresno or parts of the Central Valley, you might find policies for as low as $12-$18 per month.

These figures illustrate that renters insurance is generally a small investment for significant peace of mind, comparable to the cost of a few gourmet coffees or a single meal out, especially for those who appreciate the finer aspects of local culture and food.

Smart Strategies for Affordable Protection

Even with affordable average costs, there are several ways to further reduce your renters insurance premium without compromising essential coverage. These guides can help you maximize your savings:

- Bundle Policies: Many insurance providers offer discounts if you bundle your renters insurance with another policy, such as auto insurance. This is often one of the most significant discounts available.

- Increase Your Deductible: As mentioned earlier, opting for a higher deductible (e.g., $1,000 or $2,500) will lower your monthly or annual premium. Just ensure you can comfortably afford the deductible amount if you need to file a claim.

- Enhance Home Security: Install approved safety devices like smoke detectors, carbon monoxide detectors, fire extinguishers, and a burglar alarm system. Some insurers offer discounts for deadbolt locks or if your building has a gated entrance or security guard.

- Shop Around and Compare Quotes: Don’t settle for the first quote you receive. Obtain quotes from multiple insurance providers (e.g., State Farm, Geico, Allstate, Lemonade, Liberty Mutual, Progressive) to compare coverage options and prices. Online comparison tools can make this process quick and easy. Many reviews are available to help with this.

- Maintain a Good Credit Score: While regulated in California, a healthy credit history can still positively influence your insurance rates.

- Look for Discounts: Inquire about specific discounts. Common ones include:

- Multi-policy discount (bundling)

- Claim-free discount (for not having filed claims for a certain period)

- Non-smoker discount

- Senior discount

- Affiliation discounts (e.g., for members of certain organizations or alumni associations)

- Automatic payment discount

- Review Your Policy Annually: Your insurance needs can change. Review your policy each year to ensure your coverage still matches the value of your belongings and your lifestyle. You might have acquired more valuable items, or perhaps you’ve decluttered and need less coverage.

Beyond the Basics: Tailoring Your Policy for the California Lifestyle

Given California’s unique characteristics and the diverse lifestyles of its residents, sometimes a standard policy isn’t enough. Tailoring your coverage can provide even greater peace of mind.

Special Considerations for the Golden State

- Earthquake Coverage: Standard renters insurance does not cover damage from earthquakes. Given California’s seismic activity, many residents opt to purchase a separate earthquake insurance policy or an endorsement to their existing policy. Be aware that this coverage can be expensive and often comes with a high deductible (e.g., 10-15% of the coverage amount), but it’s a critical consideration for those living in high-risk zones.

- Flood Insurance: Similarly, flood damage is not typically covered by standard renters insurance. If you live in a flood-prone area (e.g., near the coast, rivers, or in low-lying regions), you might need to purchase a separate flood insurance policy through the National Flood Insurance Program (NFIP).

- Valuable Item Riders: For those with a collection of fine art, high-end electronics for business stays, antique jewelry, or specialized sports equipment used for activities across the state, adding a scheduled personal property endorsement is essential. This provides broader coverage and higher limits for specific items that exceed standard policy limits.

Peace of Mind for Travelers and Long-Term Renters

The transient nature of modern living, especially in a hub like California, means many individuals find themselves in temporary accommodation for extended periods or frequently traveling. Renters insurance plays a vital role here:

- Protection Away From Home: Most renters insurance policies cover your personal belongings even when they are not in your rental unit, provided they are within the policy’s specified geographic limits (often worldwide, with some restrictions). This means if your luggage is lost or stolen during a trip to Europe, or your camera is taken from your rental car while exploring Lake Tahoe, your policy might offer recourse. This is particularly valuable for frequent travelers who stay in various hotels or resorts.

- Supporting the Digital Nomad Lifestyle: For digital nomads or individuals on long-term stays in California apartments or villas, a robust renters insurance policy ensures that their essential work equipment and personal items are protected, allowing them to focus on their work and enjoy the state’s offerings without constant worry.

- Seamless Transitions: In the event of an unforeseen incident rendering a rental uninhabitable, the ALE component of renters insurance provides a financial buffer for alternative accommodation, ensuring a relatively seamless transition rather than a stressful scramble, especially for those accustomed to a certain level of comfort or structure in their travel arrangements.

In conclusion, “How much is renters insurance in California?” typically ranges from $15 to $25 per month, a small price for comprehensive protection and unparalleled peace of mind. As you explore the vast destinations, vibrant culture, and diverse lifestyles that California offers, investing in renters insurance ensures that your personal sanctuary, and everything within it, is safeguarded against life’s unpredictable moments. Don’t let the search for the perfect accommodation overshadow the importance of protecting what truly makes it home. Get multiple quotes, understand your needs, and secure your future in the Golden State.