As a premier destination for travelers worldwide, Florida beckons with its sun-drenched beaches, vibrant cities, and world-class attractions. From the magical theme parks of Orlando to the art deco charm of Miami Beach and the pristine natural beauty of the Florida Keys, the Sunshine State offers an unparalleled array of experiences. Whether you’re planning a short vacation, considering a long-term stay, or even contemplating a permanent move, understanding the local laws is crucial for a smooth and enjoyable experience. One such critical aspect, especially for anyone planning to drive, is Florida’s unique “no-fault” auto insurance system. This system, while seemingly complex, is designed to streamline the process of dealing with minor accidents and ensuring that medical bills are paid promptly, regardless of who caused the collision.

For visitors renting a car to explore the scenic routes of Highway A1A or navigating the bustling streets of Tampa, grasping the nuances of Florida’s no-fault law isn’t just a matter of legal compliance; it’s about peace of mind. It directly impacts how you would handle an unexpected fender bender or, more seriously, an accident involving injuries. Similarly, for those relocating to cities like Jacksonville or St. Petersburg, integrating into the local lifestyle includes understanding and adhering to these specific insurance requirements. This comprehensive guide aims to demystify Florida’s no-fault system, providing clarity on its implications for everyone from the casual tourist to the long-term resident, ensuring you’re well-prepared for your adventures in the Sunshine State. We’ll delve into what “no-fault” means, the essential coverage you need, and what steps to take should an unfortunate incident occur, all within the context of making your Florida experience as safe and stress-free as possible.

Understanding the Fundamentals of Florida’s No-Fault Law

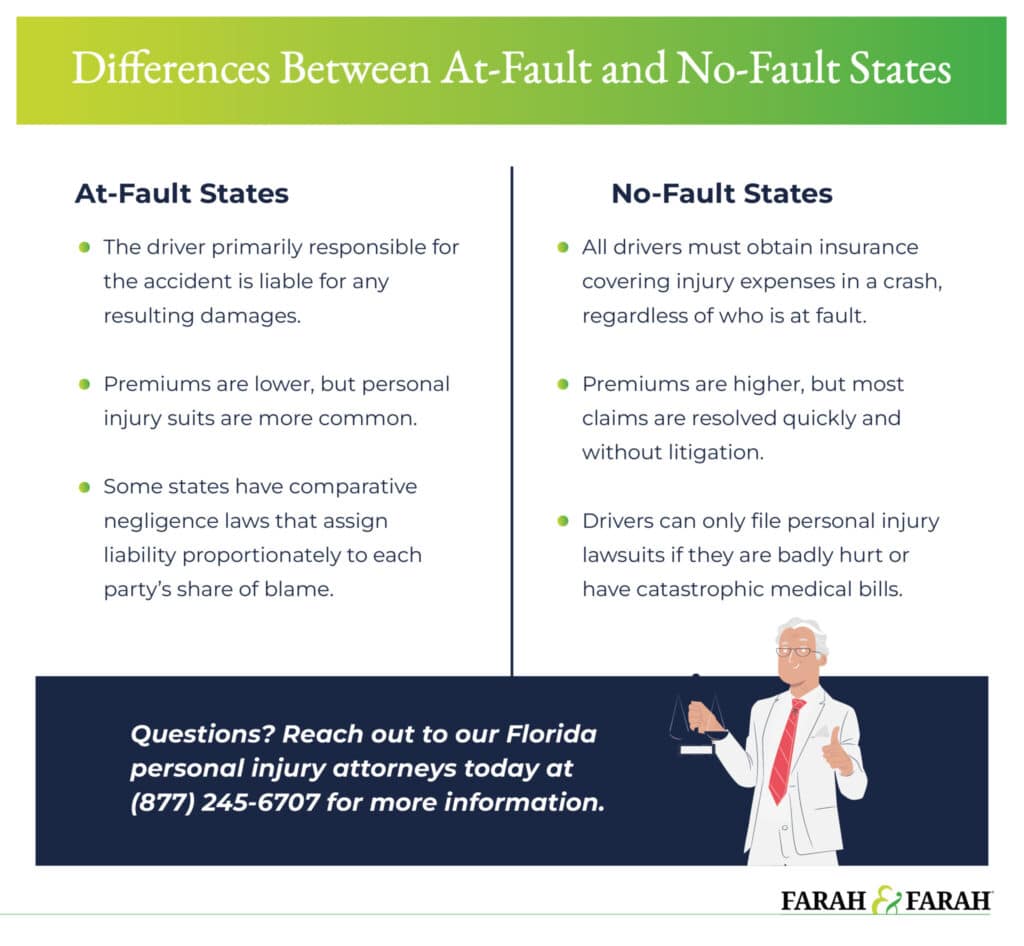

The concept of a “no-fault” insurance system can often be confusing, particularly for those accustomed to traditional “at-fault” states where liability is always a primary determinant in accident claims. Florida adopted its no-fault system to ensure that accident victims receive prompt medical care without the often lengthy and contentious process of determining who was at fault for the collision. This system is a cornerstone of vehicle ownership and operation within the state, impacting everything from insurance policy structures to post-accident procedures.

What “No-Fault” Truly Means for Drivers

In essence, a “no-fault” system means that if you’re involved in a car accident, regardless of who caused it, your own insurance company is responsible for paying your medical bills and a portion of your lost wages, up to the limits of your policy. This contrasts sharply with an “at-fault” system, where the at-fault driver’s insurance would typically cover these expenses. The primary goal of Florida’s no-fault law is to reduce the volume of minor injury lawsuits in the court system and ensure that injured parties can access necessary medical treatment quickly, thereby fostering a more efficient and less adversarial claims process for less severe incidents. It prioritizes immediate care and financial support for personal injuries, removing the immediate need to establish blame. This framework is particularly relevant for the millions of tourists who drive through the state each year, as it simplifies the initial steps following an accident, allowing them to focus on recovery rather than immediate legal battles.

The Role of Personal Injury Protection (PIP)

The linchpin of Florida’s no-fault system is Personal Injury Protection, or PIP, insurance. Every registered vehicle in Florida is legally required to carry PIP coverage. This coverage pays for 80% of necessary and reasonable medical expenses, 60% of lost wages, and 100% of replacement services (such as hiring someone to perform tasks you can’t do due to injury, like cleaning or childcare), up to a maximum of $10,000. Additionally, PIP provides a $5,000 death benefit. It’s important to note that these benefits are paid regardless of who was at fault in the accident. The intent behind PIP is to provide immediate financial relief for medical care and lost income, stabilizing the situation for accident victims. For travelers, understanding that your rental car will typically come with minimum PIP coverage is essential, but it’s also wise to verify this and understand its limitations, as $10,000 may not cover extensive injuries. This coverage ensures that whether you’re enjoying the nightlife of South Beach or exploring the historic districts of St. Augustine, your initial medical costs are addressed.

![]()

Who is Covered Under Florida’s PIP?

One of the broad advantages of Florida’s PIP coverage is its extensive reach. It doesn’t just cover the policyholder; it extends to various individuals involved in an accident with the insured vehicle. Specifically, PIP covers:

- The policyholder: The primary individual insured under the policy.

- Relatives residing in the policyholder’s household: This includes family members who live with the insured.

- Passengers: Anyone riding in the insured vehicle at the time of the accident, provided they do not have their own PIP coverage.

- Pedestrians and bicyclists: If they are hit by the insured vehicle, and do not have their own PIP coverage, they can claim benefits under the striking vehicle’s PIP policy.

- Children: Even if children are injured while riding on a school bus or other vehicle, they may be covered under their parents’ PIP policy.

This broad coverage means that if you’re visiting Florida and happen to be a passenger in a friend’s car, or even struck as a pedestrian by a Florida-insured vehicle, you would likely be covered by the relevant PIP policy for your immediate medical expenses. This aspect of the law provides an important safety net for anyone present in the state, whether as a resident, a tourist exploring the wonders of Walt Disney World Resort, or someone simply enjoying a stroll through a local park in Sarasota. It underscores the universal application of the no-fault system in addressing personal injuries arising from vehicular accidents.

Essential Insurance Requirements and Accident Procedures in the Sunshine State

Beyond understanding the theoretical framework of Florida’s no-fault system, it’s crucial to be aware of the practical requirements for drivers and the specific steps to take following an accident. These guidelines are not just legal mandates but also serve to protect you financially and medically, allowing you to focus on recovery and resuming your travel or daily life as quickly as possible. Whether you’re navigating the bustling interstates near Fort Lauderdale or the scenic coastal roads of Naples, preparedness is key.

Minimum Coverage Mandates for Florida Drivers

For all vehicles registered in Florida, state law mandates two types of insurance coverage:

- Personal Injury Protection (PIP): As previously discussed, this covers 80% of medical costs and 60% of lost wages, up to $10,000, regardless of fault.

- Property Damage Liability (PDL): This coverage pays for damages you cause to someone else’s property in an accident, up to a minimum of $10,000. This could include damage to another vehicle, a building, a fence, or other structures.

It’s vital to recognize that while these are the minimum requirements, they often provide insufficient coverage for serious accidents. For comprehensive protection, particularly in a state with high traffic volume and numerous visitors, drivers are strongly encouraged to carry additional coverage, such as Bodily Injury Liability (BIL), Uninsured/Underinsured Motorist (UM/UIM) coverage, and Collision/Comprehensive coverage. BIL protects you if you are at fault for an accident and cause injuries to others, covering their medical expenses beyond what their PIP might provide. UM/UIM protects you if the at-fault driver has no insurance or insufficient insurance. Collision and Comprehensive cover damage to your own vehicle. For new residents, securing adequate insurance from a reputable provider in Florida is a critical step in establishing a stable lifestyle in the state. Travelers renting cars should ensure their rental agreement or personal insurance policies adequately supplement the minimum state requirements.

What Happens After an Accident? The No-Fault Process

In the unfortunate event of a car accident in Florida, knowing the proper procedures is paramount.

- Ensure Safety: First, move your vehicle to a safe location if possible, and check for injuries.

- Call 911: Report the accident to the police, especially if there are injuries, significant property damage, or the vehicle is inoperable.

- Exchange Information: Collect contact and insurance information from all involved parties. Take photos of the accident scene, vehicle damage, and any visible injuries.

- Seek Medical Attention Promptly: This is crucial for your PIP claim. Under Florida law, you generally have 14 days from the date of the accident to seek initial medical treatment for your PIP benefits to apply. Failing to do so within this timeframe can jeopardize your claim for medical expenses. Even if you feel fine immediately after the crash, seeing a doctor or an emergency room for evaluation is highly recommended, as injuries may not manifest until later.

- Notify Your Insurance Company: Report the accident to your own insurance provider as soon as possible. They will guide you through the claims process for your PIP benefits.

Because Florida is a no-fault state, your initial medical expenses will be handled by your own PIP coverage, simplifying the immediate aftermath for minor injuries. This process aims to be swift and efficient, allowing individuals to access necessary care without lengthy investigations into fault, which is particularly beneficial for travelers who may have limited time in the state.

When Can You Sue? Understanding the “Serious Injury” Threshold

While Florida’s no-fault system is designed to handle most minor injury claims through PIP, it does not completely eliminate the right to sue an at-fault driver. However, to step outside the no-fault system and pursue a claim against the at-fault driver for pain, suffering, mental anguish, and inconvenience, you must meet a specific “serious injury” threshold. Florida Statutes define a serious injury as:

- Significant and permanent loss of an important bodily function.

- Permanent injury within a reasonable degree of medical probability, other than scarring or disfigurement.

- Significant and permanent scarring or disfigurement.

- Death.

If your injuries fall into one of these categories, you can pursue a personal injury lawsuit against the at-fault driver for non-economic damages (pain and suffering) and economic damages not covered by your PIP (like medical bills exceeding $10,000 or full lost wages). This threshold system aims to prevent trivial lawsuits while ensuring victims of severe accidents receive full compensation. For visitors or new residents, understanding this distinction is crucial, as it dictates when a minor incident remains an insurance claim versus when it escalates into potential litigation. It ensures that while the no-fault system handles the routine, serious cases still have recourse through the legal system, balancing efficiency with justice for victims.

Specific Considerations for Tourists, Renters, and New Florida Residents

Florida’s status as a global tourism hub means its laws often have unique implications for temporary visitors and those making it their new home. Driving is an integral part of experiencing the vastness and diversity of the state, from the serene beauty of the Everglades National Park to the bustling entertainment districts of Universal Orlando Resort. Therefore, specific guidance for these groups regarding no-fault insurance is essential for seamless travel and integration into the Florida lifestyle.

Rental Cars and Your Insurance: A Traveler’s Perspective

For the millions of tourists who flock to Florida annually, renting a car is often the preferred mode of transportation to explore attractions like Busch Gardens Tampa Bay or the vibrant streets of Key West. When you rent a car in Florida, the rental company is legally required to provide the minimum PIP and PDL coverage (typically $10,000 PIP and $10,000 PDL). This means that if you’re involved in an accident, your initial medical expenses will be covered by the rental car’s PIP policy, regardless of fault, up to the $10,000 limit.

However, relying solely on this minimum coverage can be risky. Many rental car companies offer additional insurance products, such as Liability Protection (which increases the PDL coverage and adds Bodily Injury Liability) and Loss Damage Waiver (which covers damage to the rental vehicle itself). It’s crucial for travelers to assess their existing insurance policies (personal auto insurance, credit card benefits) before accepting these add-ons. Your personal auto insurance policy from your home state or country may extend some coverage to rental vehicles in Florida, particularly for physical damage to the rental car. However, out-of-state policies often do not provide PIP coverage that meets Florida’s specific requirements. Therefore, it’s highly recommended that visitors contact their insurance provider prior to their trip to understand their coverage limitations and whether they need to purchase supplementary insurance for their Florida rental. This proactive step ensures that your dream vacation isn’t soured by unexpected financial burdens if an accident occurs.

Out-of-State Policies and Reciprocity

If you are visiting Florida and driving your own vehicle, or if you’re a new resident yet to establish Florida insurance, the question of your out-of-state policy’s validity under Florida’s no-fault law arises. Generally, if your vehicle is registered and insured in another state within the United States, your out-of-state policy may extend some liability coverage to you while driving in Florida. However, it often does not provide the specific PIP coverage mandated by Florida law for personal injuries.

This means that if you are involved in an accident in Florida while driving your out-of-state vehicle, you might not have the immediate no-fault medical benefits that a Florida resident would receive. In such scenarios, if you suffer injuries, you would likely need to pursue a claim against the at-fault driver’s insurance (if they have one) under an “at-fault” approach, or rely on your health insurance, which can be a more drawn-out and complex process. For new residents, it is absolutely essential to switch to a Florida auto insurance policy with the mandatory PIP and PDL coverage as soon as you register your vehicle in the state. Failing to do so can result in severe penalties, including fines, license suspension, and registration revocation. Planning your move includes thorough research into state-specific legal requirements to avoid any disruptions to your new lifestyle.

Protecting Yourself: Key Tips for Driving in Florida

Whether you’re a seasoned traveler or a new resident, adopting safe driving practices and understanding key protective measures in Florida is invaluable.

- Stay Informed: Familiarize yourself with local traffic laws and road signs. Florida highways can be congested, especially around major tourist attractions.

- Maintain Adequate Insurance: While minimum coverage is legally required, consider higher limits for PIP and PDL, and add Bodily Injury Liability and Uninsured/Underinsured Motorist coverage. The peace of mind this extra protection offers is invaluable, especially when exploring new areas or commuting daily.

- Drive Defensively: Be aware of other drivers, as Florida has a diverse mix of local, national, and international drivers, all with varying driving habits. Pay particular attention in areas known for heavy tourist traffic, such as International Drive in Orlando or the causeways leading to Miami Beach.

- Know What to Do After an Accident: Always remember the 14-day rule for seeking medical attention to activate your PIP benefits. Exchange information, take photos, and report the accident to your insurer promptly.

- Secure Your Rental Agreement: If renting a car, thoroughly review your rental agreement and understand the insurance options presented. Clarify what your existing insurance covers and what supplemental coverage you might need for your specific trip to Florida.

By proactively addressing these aspects, you can ensure that your experience driving in Florida remains enjoyable, whether you’re embarking on a leisurely road trip through the historic towns of the Panhandle or settling into a new community in the vibrant heart of the state.

Florida’s No-Fault System in the Broader Context of Travel and Lifestyle

Florida’s no-fault auto insurance system, while primarily a legal and financial construct, profoundly impacts the travel and lifestyle experience in the state. Its underlying philosophy of ensuring prompt medical care and reducing litigation for minor injuries aligns with the state’s image as a hassle-free vacation destination and a welcoming place to live. When planning a trip or considering a move, understanding such foundational laws contributes significantly to a sense of preparedness and confidence.

For travelers, the knowledge that initial medical bills following a minor car accident will be covered by their own or the rental car’s PIP can alleviate a significant source of stress. This allows visitors to immerse themselves fully in Florida’s abundant offerings, from the serene beaches of Siesta Key to the thrilling rides at SeaWorld Orlando, knowing that a foundational safety net is in place. It transforms a potentially daunting legal detail into a practical assurance, enhancing the overall quality of their travel experience. Travel guides and accommodation providers often emphasize safety and preparedness, and understanding Florida’s no-fault system is an integral part of this advice, ensuring tourists can focus on creating unforgettable memories rather than worrying about potential legal complexities.

Similarly, for new residents, grasping the nuances of PIP and PDL is a crucial step in integrating into the Florida lifestyle. It’s part of establishing a secure and responsible presence in the community, much like finding the right housing, understanding local taxes, or enrolling children in schools. The no-fault system is not just about insurance; it’s about participating in a civic framework designed to manage risk efficiently. Budgeting for adequate insurance coverage becomes a key component of financial planning for a move, ensuring that their new life in Florida, whether it’s in a bustling metropolitan area like Miami or a quieter coastal town, remains stable and secure.

Ultimately, Florida’s no-fault auto insurance system is a reflection of the state’s approach to public safety and convenience. By prioritizing quick resolution of minor injury claims, it helps maintain the flow of life and commerce, crucial for a state heavily reliant on tourism and a growing population. Whether you are seeking luxury travel, budget-friendly adventures, family trips, or business stays, being well-informed about driving laws contributes to a more informed and worry-free engagement with all that the Sunshine State has to offer. It’s an often-overlooked yet vital piece of the puzzle for anyone looking to fully enjoy their time in Florida.